Proposal seeking to allocate up to 70,000 wNXM from the Community Fund to the wNXM Bancor pool, assuming space is opened up in the pool. There is a proposal on the Bancor governance to increase the space to 10M BNT (~$25m of space for wNXM to be staked) gradually, 1M increment at a time.

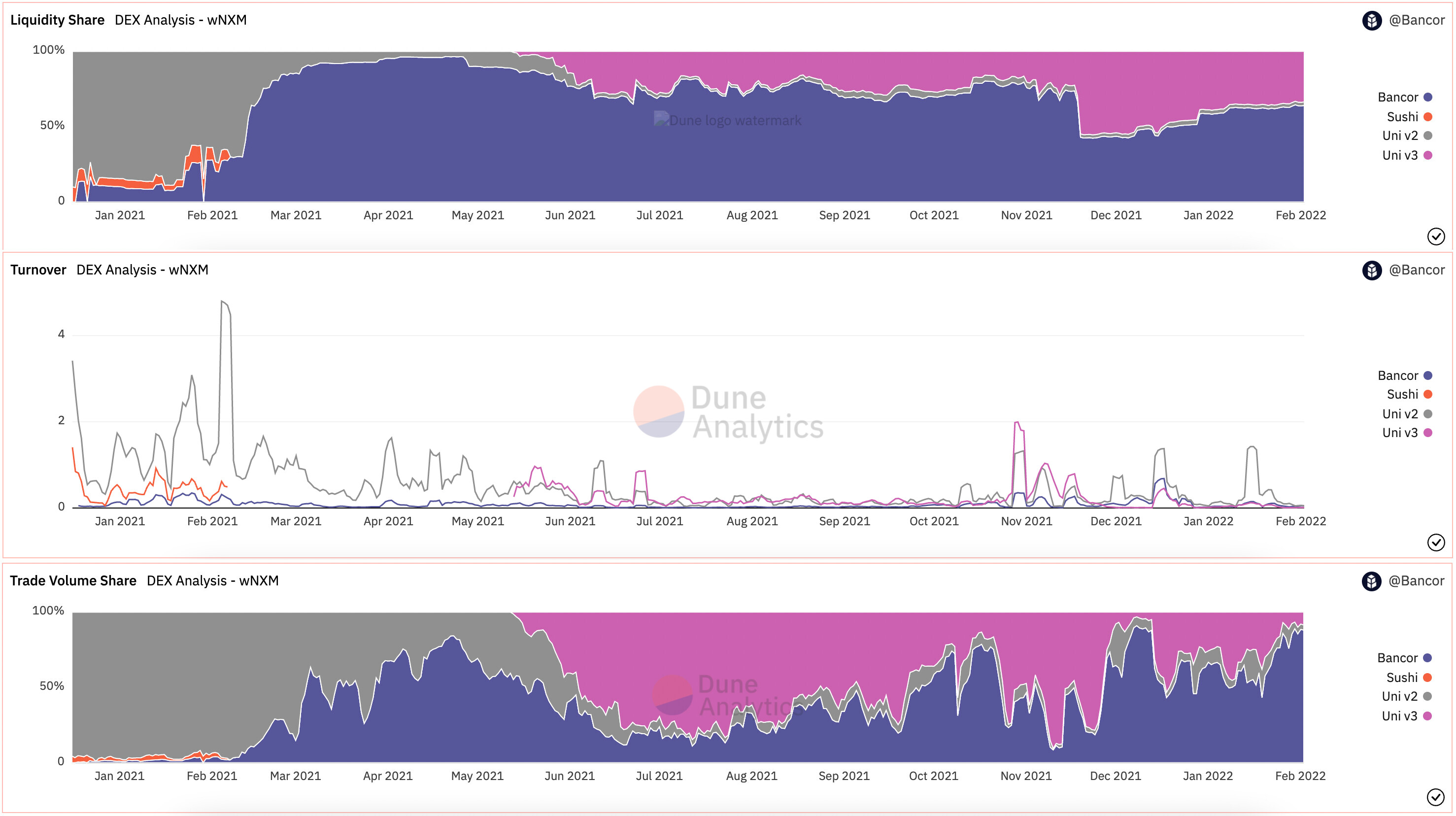

Yields have been in the range of 2 - 15% over the last 2 weeks. Data on Liquidity Share, Turnover, and Trade Volume is presented.

Full impermanent loss protection provides a safe way for the Community Fund to earn additional yield on some of its idle assets.

Bancor’s contract safety, single-sided staking and some upcoming Bancor 3 phase 1 features are especially interesting for a fund deposit.

Figure 1 - wNXM Liquidity Share, Turnover and Volume Share since the beginning of 2021 [1].

Advantages of deploying on Bancor

Single-sided staking

Provide liquidity with only wNXM and get all the benefits of liquidity provision without ever selling a single wNXM token.

100% IL protection

Impermanent loss protection scales up with time on Bancor v2.1 but will be instantly provided on Bancor 3. Liquidity migration to Bancor 3 from Bancor v2.1 will immediately accrue 100% IL protection.

Furthermore, Bancor 3 Phase 1 (of 3) will offer several interesting features for LPs, especially for treasuries:

Auto-compounding TKN rewards and fees

Limitless pools with single-sided staking

Instant Impermanent Loss protection

LP tokens - they represent a share of the pool’s liquidity+fees+rewards, which grows with time, making them an ideal collateral.

More broadly to this specific opportunity I believe we need to more actively manage the Community Fund treasury ~240,000 NXM (outside of buyback funds). This could involve many different opportunities/strategies, as well as discussions on allocating some funds to stables etc, but there will always be a large portion of the fund held in NXM/wNXM. Earning some yield on this is obviously beneficial for the Nexus ecosystem and will allow more grants/hub based team to be funded.

At present there are very few yield earnings opportunities for NXM (outside staking on Nexus) that don’t incur impermanent loss and providing liquidity on Bancor is likely the only one that can be done at any reasonable scale. In addition, extra DEX liquidity for NXM does have some wider benefits as it may attract larger capital allocators to the Nexus ecosystem.

Overall, I’m supportive of this proposal assuming the corresponding proposal to increase space in the wNXM pool is successfully passed via Bancor governance.

Great proposal but only makes sense once wNXM trades above book, and best case decently above it, because it deepens the liquidity. So it could actually make a ton of sense to start depositing wnxm of the treasury at the end of another buyback, if it would pass.

Ultimately agree that liquidity should increase… but in my view doesn’t make sense to do so right now at a huge discount to book value (~80% upside to book), because that would increase the likelihood that wnxm stays below book value. It would make sense to begin increasing it at book value and than increasingly on the path back to the bonding curve and native exchange and swap through nexus directly

ultimately my arguments goes that the mutual and long-term aligned members should buy all tokens it can get below book… and that we should “stabilize” the price around and over book value for $wnxm… imo its not a healthy signal if $wnxm trades with massive liquidity 50% below book…

This has some real DPI buying vibes to it - I am open to being convinced but locking a third of the community fund permanently into Bancor doesn’t seem like a great idea while we are trading at a discount. Tokemak makes much more sense imo - we can just get Delphi to vote us a reactor. Or we could go the Curve route and make a ETH/WNXM pool and bribe votes through votium and/or use Olympus Pro to bond in CVX for WNXM. Balancer another option etc. Can we fund someone to do an analysis of the options available and their pros and cons?

Thank you for your feedback. A couple of comments after reading some replies:

A wNXM stake on Bancor benefits from single-sided staking. This means that no wNXM from the treasury is sold to stake in the Bancor pool. Selling this much wNXM would put a downward pressure on the price and decrease capital efficiency of the treasury funds.

The wNXM is protected against Impermanent Loss, with Instant Impermanent Loss protection coming with B3 (every stake migrated from Bancor v2.1 will immediately get 100% protection).

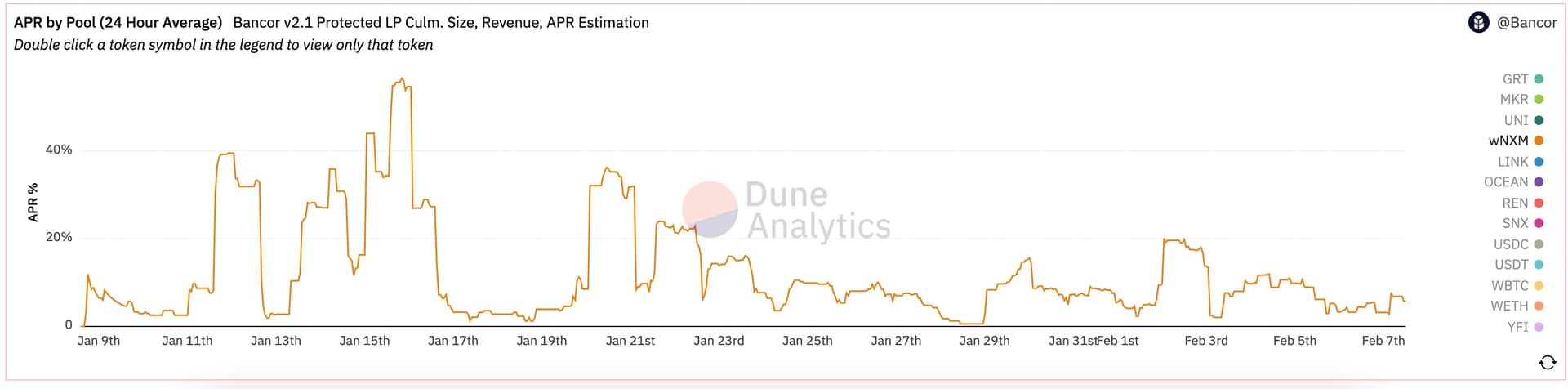

The wNXM pool has been one of the best performers on Bancor, APRs in Figure 1.

The proposal was written so that, if the DAO wishes to stop staking on Bancor, the trading liquidity limit increases will stop as well.

I highly recommend joining the community chat between Bancor and Nexus Mutual that will happen on the 8th February (tomorrow) at 3pm GMT, where all these questions and more can be addressed by Mark Richardson, our Head of Research!

Agree that something like Tokemak or Ohm buying up wnxm would be the best to put buy pressure onto wnxm… but still agree that bancor is a great option for us to increase liquidity on wNXM once we are at higher prices relative to book value