Introduction

This report summarises karpatkey’s activities and achievements in November 2024, with the focus on selling and diversification of NXM Token.

Financial Results

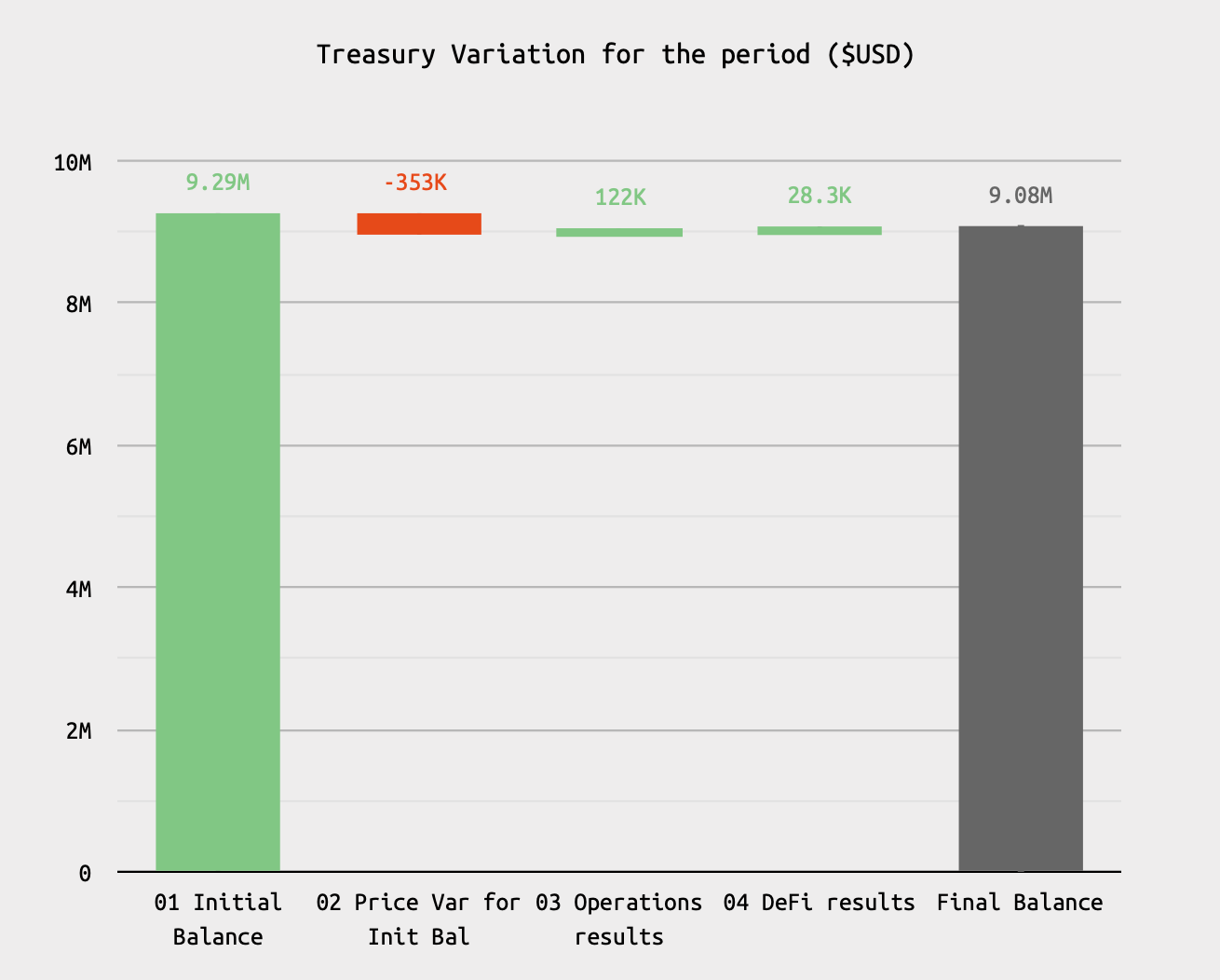

- The treasury has increased from $6.68 million at the end of October to $9.28 million as of the end of November.

- The revenue generated from protocol fees to the treasury amounted to $83.3k in November.

- Treasury allocation to DeFi activities stands at 34.3%.

- Detailed information about the treasury results is available in the November report, accessible via the dedicated Nexus Mutual dashboard on the Karpatkey website.

Treasury Operations

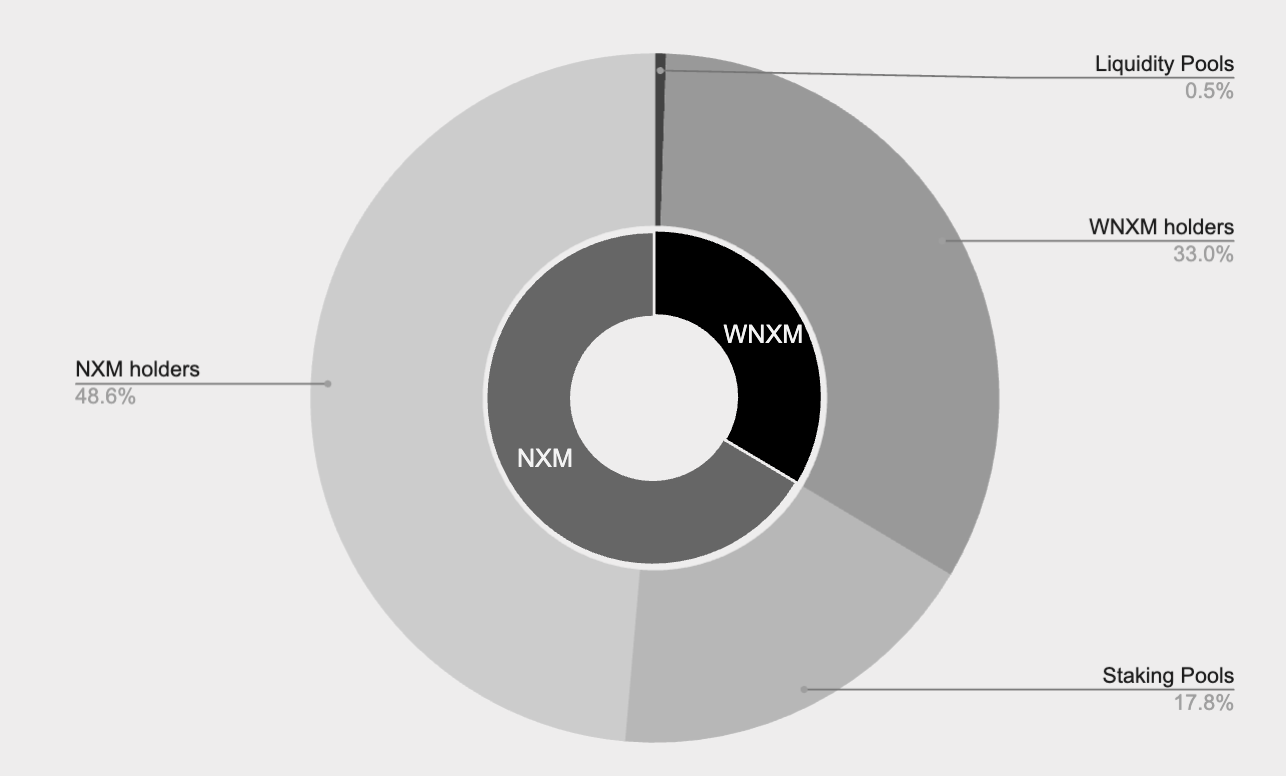

NXM Staking

-

As part of the mandate from the Nexus Mutual DAO treasury, 100% of the NXM earmarked for the staking program (35,803.80 NXM) has been allocated across five staking pools. The allocation strategically balanced exposure between high and low-claim-rate products to maximize returns while mitigating the risk of over-staking, thereby safeguarding the pool’s APY.

-

An additional 10,200 NXM was staked to improve capital efficiency in the context of prices below book value and slow redemption process, which limits the immediate usability of unwrapped NXM.

-

To encourage cover purchases, the overall staking period was extended by 91 days to 23rd April 2025.

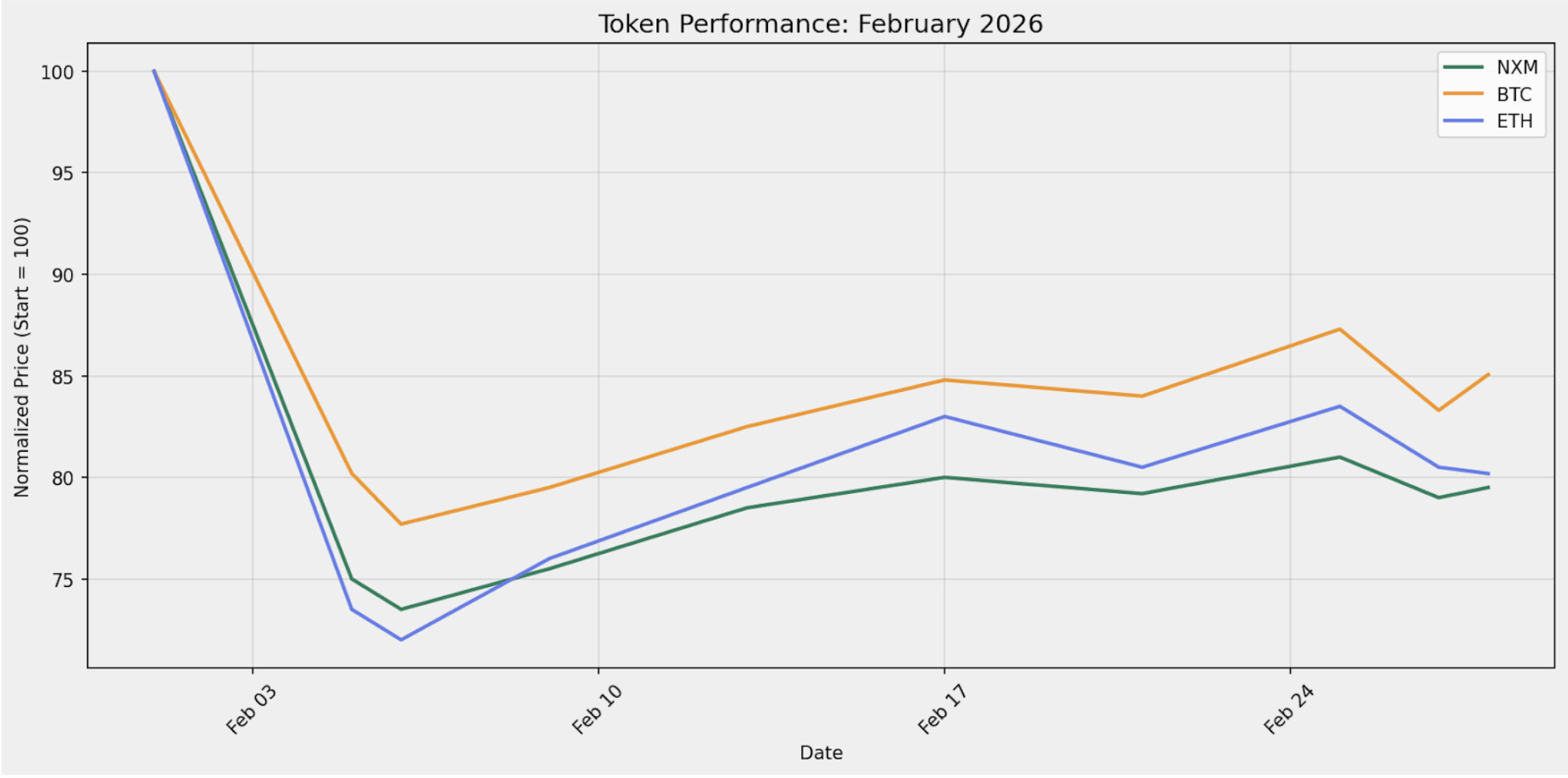

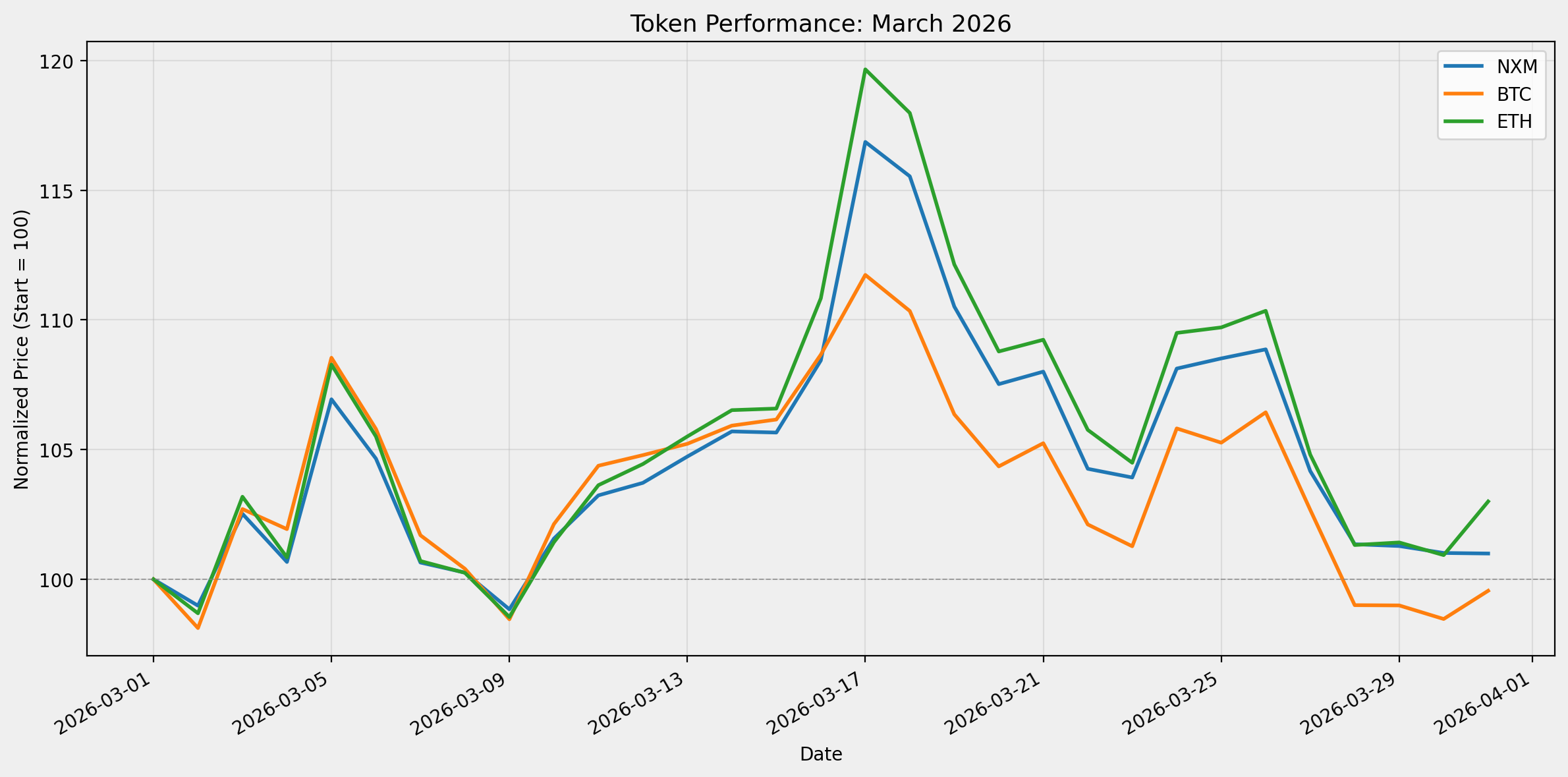

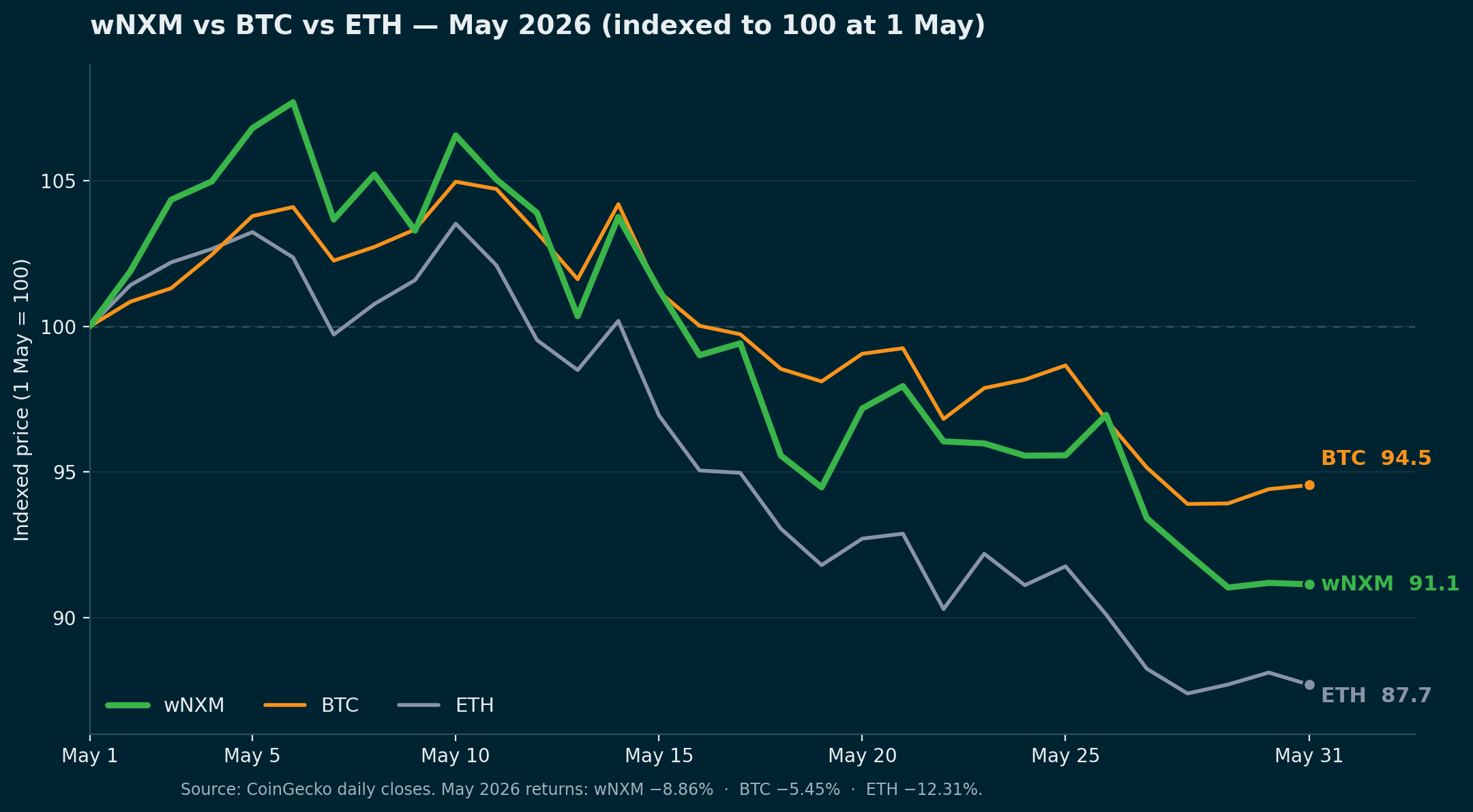

NXM Selling

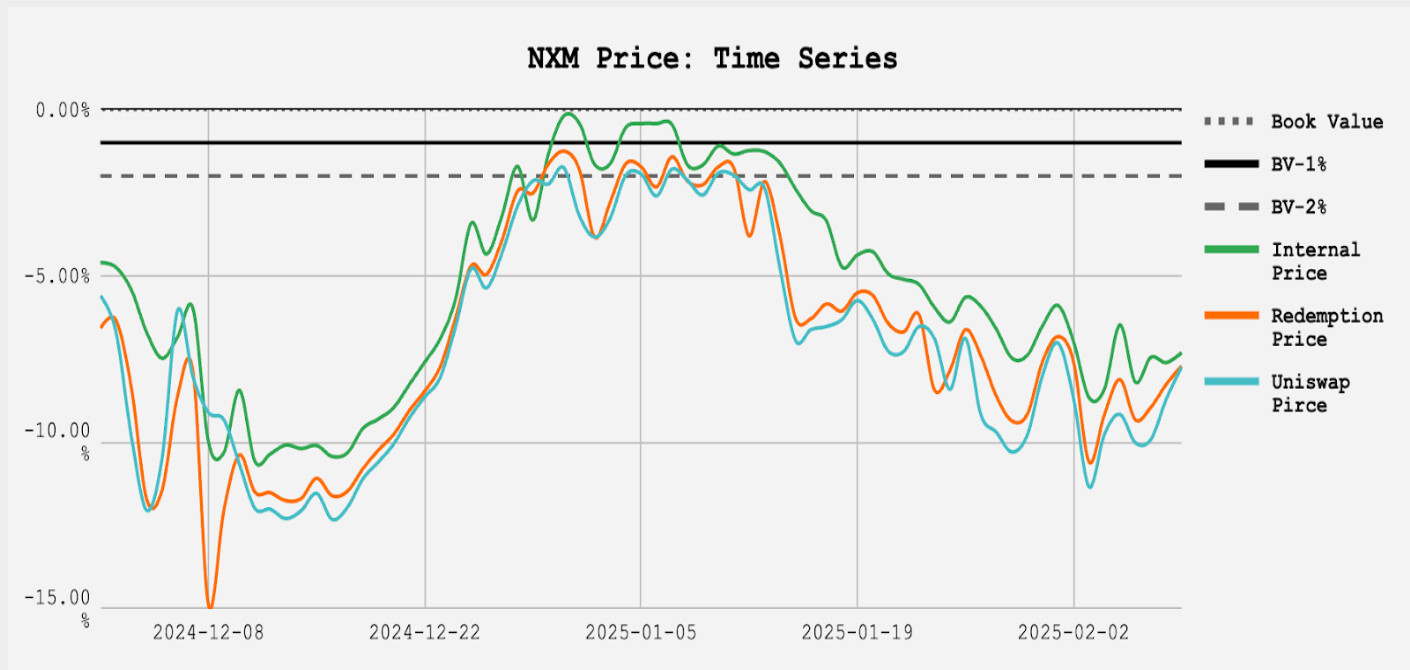

- An amount of 2,000 NXM were swapped at spot price, staying within the aligned 1% of the redemption price.

- Selling was paused in the last week of November to protect Nexus Mutual’s financial interests, as the spot price showed a significant deviation from the book value.

- By not selling NXM well below book value, karpatkey ensures the treasury’s value is preserved, avoiding unnecessary devaluation of Nexus Mutual assets.

- Moving forward, karpatkey will closely monitor the deviation and only resume selling in line with the 1% mandate, maintaining a responsible and professional approach to treasury management.

Liquidity provision

-

Two positions have been created in the WNXM/WETH V3 pool on Uniswap: one with a tighter range for improved capital efficiency and another with a broader range to better capture price volatility.

-

Both positions are currently out of range but have accrued significant swap fees (~$3,288). The broader range is designed to ensure liquidity availability during periods of high price deviation, while the tighter range optimizes earnings during periods of stability.

-

ETH Derivative

As a part of mandate, WETH resulting from wNXM diversification was allocated to wstETH to gain exposure to ETH staking yield. The Nexus Mutual treasury now holds ~30 wstETH, and we plan to increase our exposure to ETH derivatives as the price improves.

Next Steps

- Explore WNXM/USD pools on CoWAMM.

- Adding new Zodiac Permissions so that CoWAMMs can be incorporated, which is now insured by Nexus Mutual.

- Actively monitor the NXM price to continue the diversification process.