NMPIP 239: Onboard cbBTC as a Capital Pool Asset

- Open for Voting: NMPIP 239

- Voting Period: 17 October 3pm UTC until 20 October 3pm UTC

Overview

On 12 September 2024, Coinbase launched Coinbase Wrapped BTC (cbBTC), a BTC derivative that is backed 1-to-1 with BTC held in custody by Coinbase. Onboarding cbBTC as a Capital Pool asset would present the Mutual with a competitive advantage as the Foundation and DAO teams look to expand into new lines of business and appeal to a broader audience of crypto-native users.

On behalf of the Product & Risk team, I am proposing Nexus Mutual members vote to onboard cbBTC as a Capital Pool asset and grant the Advisory Board the power to complete the three (3) stages of onboarding:

- Stage 1: Onboard cbBTC as an asset in the Capital Pool

- Stage 2: Swap ETH for cbBTC (initial amount of $1M)

- Stage 3: Enable cbBTC-denominated cover buys at user interface (UI) level

Rationale

cbBTC Overview

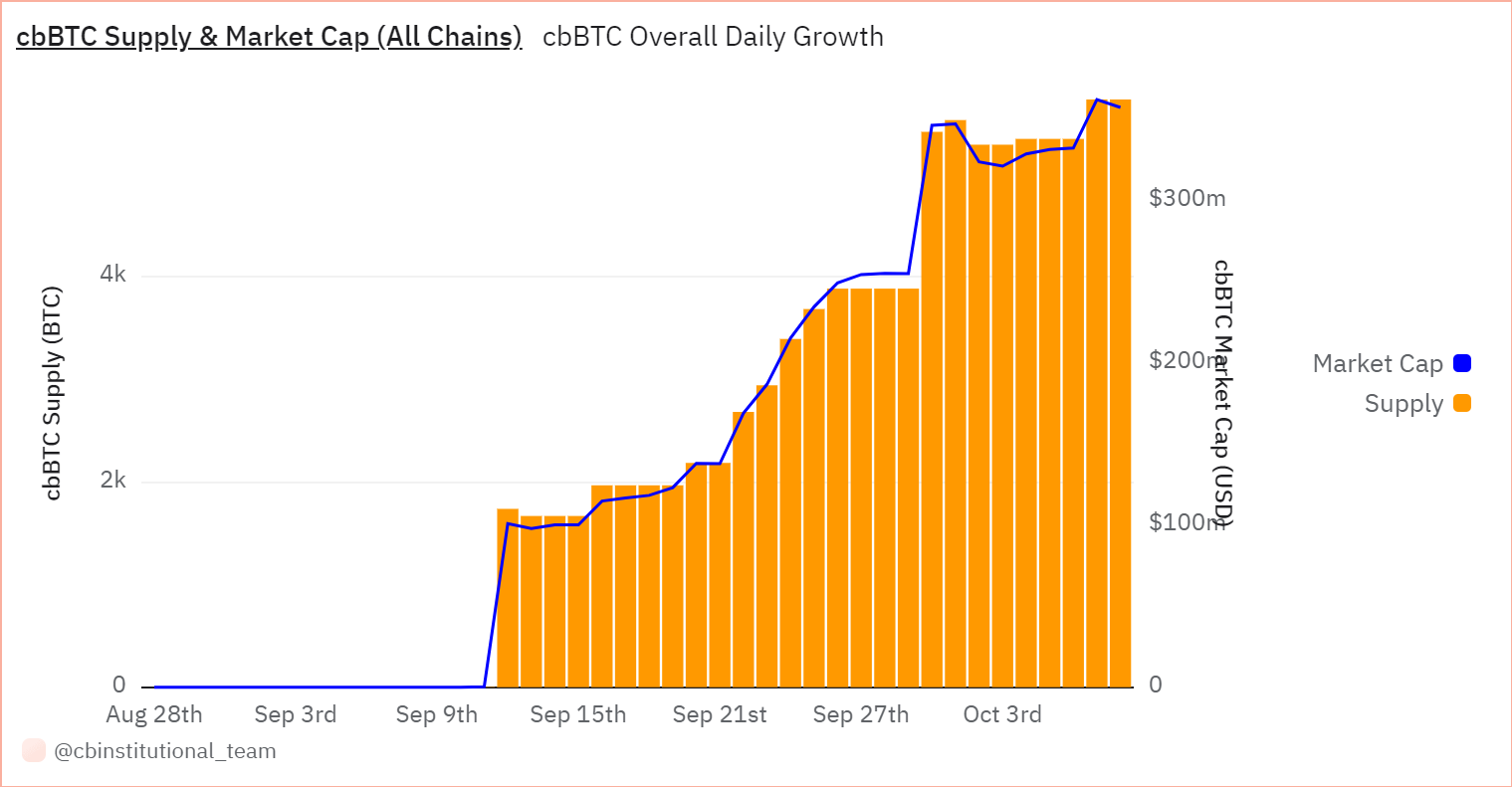

cbBTC has grown to 5,731 BTC ($357.5M Market Cap) in a matter of 26 days since its initial launch. In under one (1) month, cbBTC has climbed the Bridge TVL rankings into the top 10, if it were listed on DefiLlama.

Source: cbinstitutional_team Coinbase Wrapped Bitcoin (cbBTC) Dune dashboard

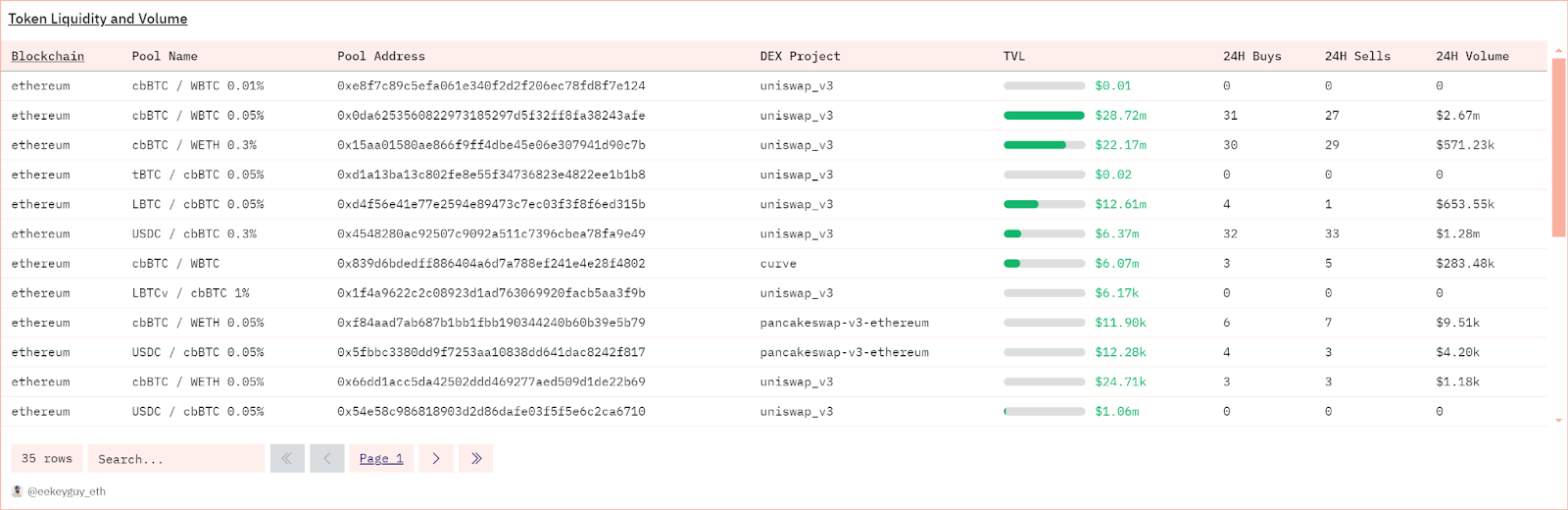

Onchain liquidity for cbBTC has grown quickly, as well, with $77M+ worth of cbBTC liquidity established on Ethereum, primarily in three (3) Uniswap v3 pools. Of course, cbBTC can be minted and redeemed directly on Coinbase by users and can be traded on the exchange, as well. Between onchain liquidity and the mint/redeem function on Coinbase, there’s sufficient liquidity to acquire and hold a minimum of $1M in cbBTC in the Capital Pool.

Source: eekeyguy_eth’s Coinbase Wrapped BTC (“cbBTC”) Dune dashboard

cbBTC is poised for growth at the institutional layer and across DeFi, as major lending protocols have or are working to onboard cbBTC to their markets. Given Coinbase is the primary custodian for both the BTC and ETH ETFs, there’s a high likelihood that cbBTC’s market share will grow substantially by the end of 2024.

In the following sections, I’ll go into detail regarding the following:

- The business case for onboarding cbBTC to the Capital Pool

- The risks associated with onboarding cbBTC as a Capital Pool asset

- The rationale for not pursuing other BTC derivatives

Business Case for Onboarding cbBTC to the Capital Pool

Nexus Mutual is the only insurance alternative that offers claim payments in crypto-native assets. Even traditional insurers pay claims denominated in fiat terms. This has been and remains one of the Mutual’s core strengths compared to other onchain cover providers and traditional insurers.

Onboarding cbBTC as a Capital Pool asset would present the Mutual with a competitive advantage as the Foundation and DAO teams look to expand into new lines of business and appeal to a broader audience of crypto-native users.

While many users purchase ETH-denominated covers to protect volatile crypto assets other than stablecoins, BTC and BTC derivative holders want to receive a potential claim payment in BTC terms, not ETH terms.

Offering members the ability to purchase cbBTC-denominated covers and receive claim payments in cbBTC would open the door to new lines of business and help the Mutual further scale cover sales according to our core growth objective.

I’ll review the business cases for onboarding cbBTC to the Capital Pool below.

Appealing to Crypto-Native & Institutional Users Primarily Holding BTC

Since the Bitcoin ETFs launched earlier this year, the BTC ETFs have amassed more than $60B of BTC, or 4.83% of the total BTC supply. There’s now an institutional audience that can gain exposure to BTC and learn more about BTC’s utility. Greater awareness among institutional investment firms such as BlackRock, Fidelity, Franklin Templeton and others will result in greater institutional adoption of BTC.

Naturally, institutional investors who decide to custody BTC themselves will want to evaluate additional yield strategies for their BTC holders. This presents a massive future market opportunity for the Mutual.

In the short-term, the Mutual can appeal to BTC holders looking to earn yield on their BTC using BTC derivatives such as WBTC, tBTC, cbBTC, and others. The major BTC derivatives (i.e., WBTC, Binance BTC, SolvBTC, tBTC, uniBTC, and cbBTC) represent ~$15.5B, or 1.24% of the BTC supply. By onboarding cbBTC to the Capital Pool, the Mutual can appeal to these holders who currently, or who plan to, deploy their BTC derivatives across DeFi.

Major lending protocols such as Aave, Morpho, Compound, and Euler have onboarded cbBTC as collateral in their markets, and many other BTC derivatives are already enabled or have recently been added as collateral on those lending markets, as well.

cbBTC-denominated covers would be a first for any onchain or offchain market.

Underwriting Cover for BTC Mining Operations

BTC mining operations have limited access to traditional insurance based on the nature of their business. Due to this, the underwriting capital is quite limited and BTC mining businesses cannot access the coverage they need to safeguard against service interruptions or other loss events.

Onboarding cbBTC to the Capital Pool would allow the Mutual to tap into this capital-starved market and further scale cover sales. The Mutual would also be the only cover provider in the market offering BTC-denominated cover to these businesses. This could result in a tangible growth in cover sales and premiums for the Mutual.

BTC Restaking Market Opportunity

The Mutual’s core product offerings (i.e., Protocol Cover, Bundled Protocol Cover, Native Protocol Cover, Fund Portfolio Cover, and DeFi Pass Cover) are yield-driven products. As yields rise, cover buy volume increases and the Mutual’s active cover amount achieves growth. The Mutual has focused on Ethereum and EVM-compatible networks primarily because yield opportunities in DeFi are present in these ecosystems.

With the introduction of restaking across Ethereum and Bitcoin networks, there are now yield opportunities available to BTC holders outside of standard DeFi yields. The growth in yield opportunities for BTC derivatives opens up a potential new line of business for Nexus Mutual based on smart contract and slashing risk.

Given the new capital flowing into BTC and the existing market segment of BTC holders with no access to BTC-denominated coverage, the BTC restaking market could also provide the Mutual with a first-mover advantage.

Risks Associated with Onboarding cbBTC as a Capital Pool Asset

Onboarding cbBTC would allow the Mutual to tap into new markets, user segments, and lines of business. However, this decision comes with additional risk. In this section, I’ll review the core risks associated with onboarding cbBTC to the Capital Pool.

For third-party reviews of cbBTC’s risks, see the analysis provided by Block Analitica on the MakerDAO forum in this thread; Chaos Labs analysis on the Aave forum; and LlamaRisk analysis on the Aave forum.

Below is an independent assessment of the risks outlined by the Product & Risk team. Be sure to review the available information and make an informed decision based on your own research pending any onchain vote. If you have questions or concerns, please voice them in the comments section of this forum post.

Counterparty Risk

cbBTC is backed 1-to-1 with BTC held in custody on the Coinbase exchange. While Coinbase is a centralized exchange, it is a publicly traded company and is the primary custodian of choice for both the BTC and ETH ETF issuers.

To mint and redeem cbBTC, one must be a Coinbase user in good standing, per clause 7.1 of the Coinbase User Agreement. cbBTC holders maintain ownership of the underlying BTC held on Coinbase, per clause 7.1.5. of the Coinbase User Agreement. When cbBTC is sold or transferred, the ownership rights to the underlying BTC also transfer with the cbBTC, per clause 7.1.4. of the Coinbase User Agreement. LlamaRisk has already confirmed that in the event of a Coinbase bankruptcy event, cbBTC holders “…can assert ownership over custodied BTC. These assets are protected from Coinbase’s bankruptcy estate and third-party claims, as they don’t become Coinbase property and are legally insulated from Coinbase’s creditors.”

While Coinbase is a well-regarded and trusted custodian, counterparty risk exists with any centralized custodian. Proof of Reserves (PoR) is not yet enabled for cbBTC, and it is not guaranteed that a PoR onchain feed will be provided in the future. Despite these issues, counterparty risk for cbBTC is on par with the counterparty risk associated with Circle’s USDC and doesn’t provide a blocker for onboarding cbBTC to the Capital Pool based on the Product & Risk team’s independent review.

While regulatory risk is uncertain in the US, Coinbase has operated a centralized crypto exchange for more than a decade and is the custodian of choice for both BTC and ETH ETFs and other institutional players. Coinbase Custody Trust Company, LLC does not appear to be the subject of any investigation or enforcement action, so regulatory risk, while uncertain, remains on par with the regulatory risk of onboarding WBTC or any other centralized BTC derivative.

Market Risk

cbBTC is an emerging asset in the market. While it has seen significant growth since launch and has maintained its peg with BTC, cbBTC has the potential to fluctuate in price and potentially depeg from the market price of BTC. The ability to mint and redeem cbBTC on the Coinbase exchange and the growing TVL in onchain liquidity pools for cbBTC can provide significant liquidity for redemptions, selling, and arbitrage between onchain and offchain markets.

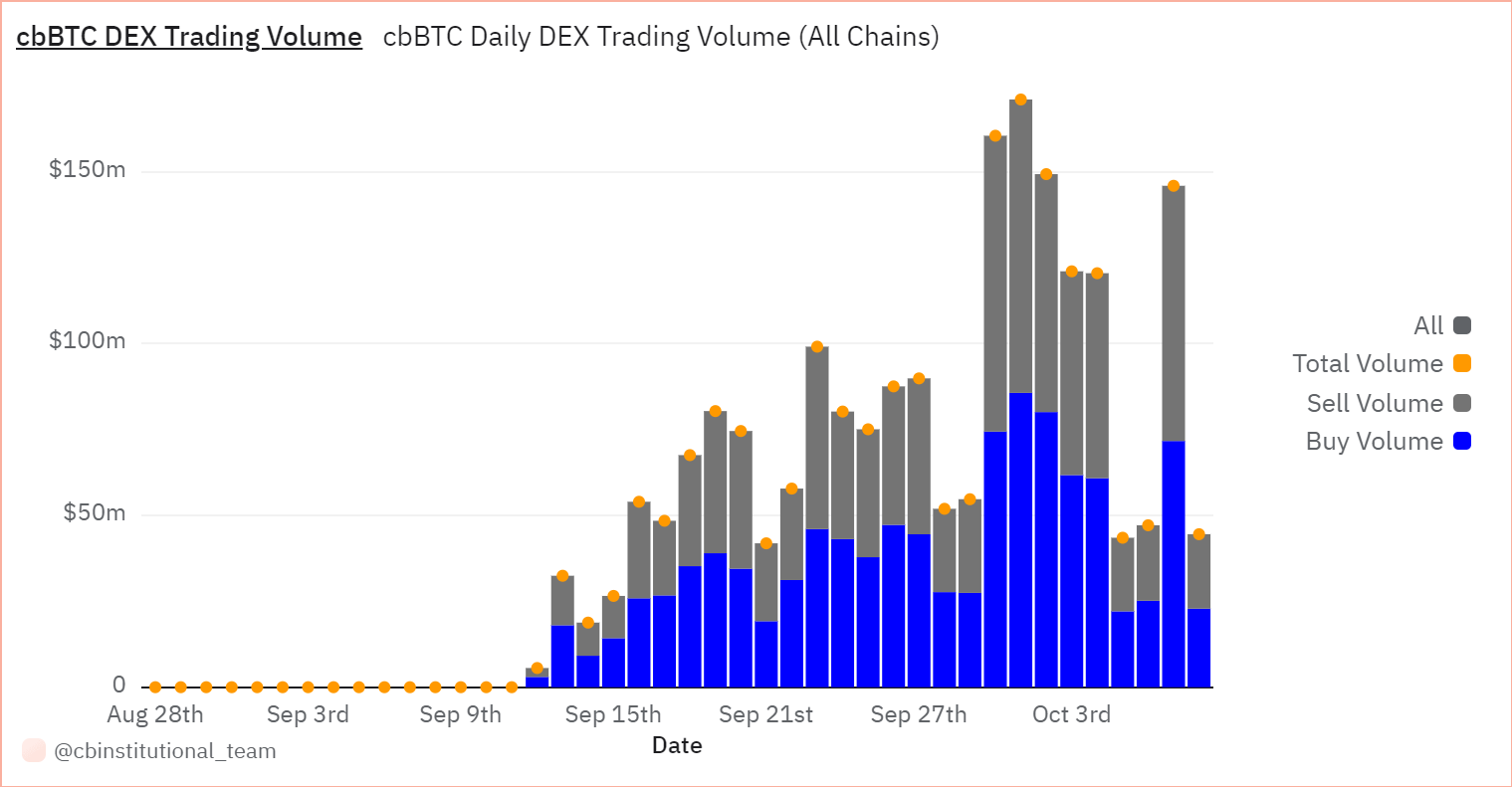

To date, 1196 cbBTC have been redeemed for the underlying BTC. Sell and buy volume has been consistent, with the highest day of sell volume at $86.13M on 30 September. The majority of trading has occurred through Aerodrome on Base, while Uniswap v3 has seen the largest trade volume on Ethereum.

Source: cbinstitutional_team Coinbase Wrapped Bitcoin (cbBTC) Dune dashboard

Source: cbinstitutional_team Coinbase Wrapped Bitcoin (cbBTC) Dune dashboard

While the risk of a cbBTC depeg is present, the Product & Risk team does not believe this is a significant blocker to onboarding cbBTC to the Capital Pool.

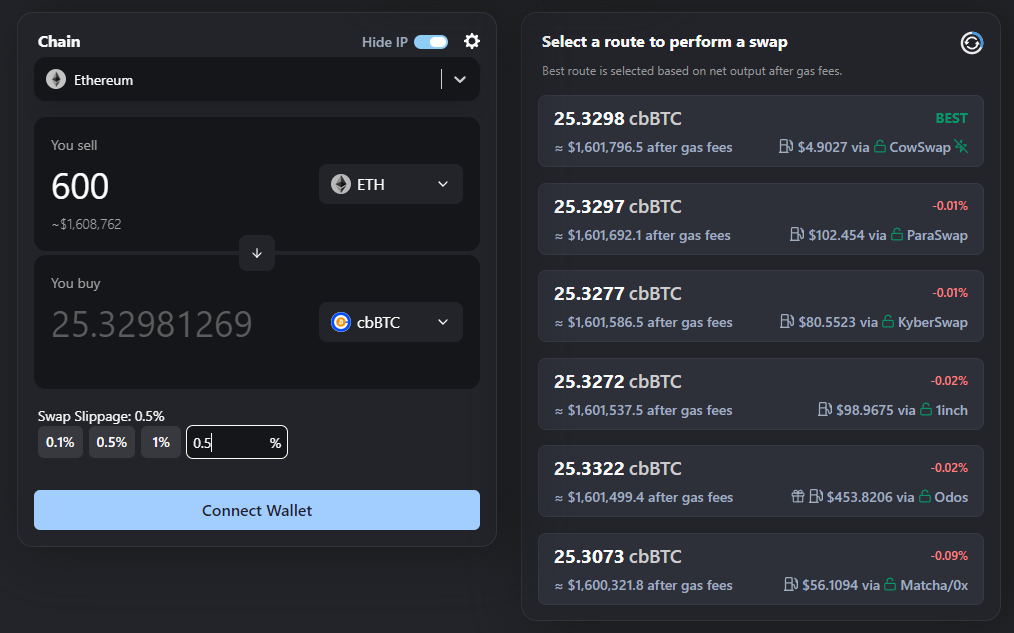

At current exchange rates, the Mutual could acquire 600 ETH worth of cbBTC with less than 0.5% slippage, according to a quote on LlamaSwap. A quote on 1inch yield similar results with slippage quoted at 0.31% for a 600 ETH swap into cbBTC. For the Mutual’s purposes, any potential swaps could be executed in smaller sizes to ensure minimal slippage when adding cbBTC to the Capital Pool.

Because cbBTC will represent a small percentage of the overall Capital Pool and a depeg event has a low likelihood of occurring, the risk appears to be minimal at present.

Smart Contract Risk

cbBTC uses the same codebase as cbETH, which has been live since 2022. The codebase has been audited by OpenZeppelin and hasn’t seen any hacks or other security-related issues since its launch. Coinbase also provides ample incentives for whitehat hackers to review their codebase and responsibly disclose any critical vulnerabilities for rewards of up to $1M through their bug bounty program.

The Product & Risk team finds the smart contract risk level for cbBTC to be low, or an acceptable level for onboarding cbBTC to the Capital Pool.

Oracle Risk

Nexus Mutual’s NXM token is backed by assets held in the Capital Pool. When onboarding new assets to the Capital Pool, a reliable oracle is a core requirement to ensure NXM price calculations are accurate. This is crucial given quotes for cover, staking rewards, minting new NXM through the RAMM or redeeming NXM through the RAMM, etc. all require an accurate NXM calculation.

For crypto-native assets, the Mutual prefers to use Chainlink oracles. Fortunately, Chainlink has launched a cbBTC/USD oracle on Ethereum mainnet. The deviation threshold for this oracle is 2% and the heartbeat timeframe is 24 hours (86,400 seconds), which is higher than the other Chainlink oracles the Mutual uses to calculate the NXM price. However, the Mutual will maintain a heavy majority of the Capital Pool in ETH and only hold the minimum required amount of cbBTC ($1M). This can be revisited if the Mutual’s exposure to cbBTC grows significantly in the future, pending an approval to onboard cbBTC to the Capital Pool.

The price deviation threshold for this oracle is higher than desired, but given cbBTC will represent a minor position in the Capital Pool and the division threshold and heartbeat can be updated as cbBTC matures, the Product & Risk team finds the oracle risk to be acceptable to onboard cbBTC to the Capital Pool.

Rationale for Not Pursuing Other BTC Derivatives

Wrapped BTC

While Wrapped BTC (WBTC) is significantly larger than cbBTC, the announcement from BitGo in August stating they would be moving WBTC’s ownership to BiT Global has sparked concern about the integrity of the WBTC product and its future in the market. After this news broke, monetsupply on behalf of Block Analitica Labs posted a proposal on the Sky Money forum to offboard WBTC from Sky Money’s vaults and the SparkLend markets. There has been back-and-forth on the Sky Money forum regarding this proposal, but it has moved forward.

Other major lending protocols have discussed the changes in WBTC’s risk profile. Most notably, Chaos Labs has proposed “…decreasing supply and borrow caps for all WBTC markets to a level 5-15% higher than current utilization. This ensures that users can still manage the health of their WBTC collateral positions while limiting market growth. This is a critical change to manage Aave’s exposure to WBTC.” This is based on their finding that “…the material risk of WBTC has changed, given its new jurisdictional set up, which may increase regulatory risk, as well as its new “strategic partnership” with Justin Sun, which may increase counterparty risk.” The onboarding on cbBTC and tBTC as assets in select Aave markets shows that the leading lending protocol is moving to diversify their exposure to BTC derivatives while there’s uncertainty about WBTC’s future risk profile.

Due to this uncertainty, the Product & Risk team does not find it prudent to onboard WBTC at this time. It is possible that major lending protocols continue to limit exposure and reduce WBTC’s use as collateral over time, while cbBTC’s market share grows beyond its current 6.2% level (Source: cbinstitutional_team’s cbBTC Market Share Over Time Dune dashboard).

Threshold tBTC

In December 2021, the Keep and NuCypher communities voted to approve a merger between these two protocols, which created the Threshold Network and the latest version of tBTC. Since this merger, tBTC has offered BTC holders with a decentralized bridge that allows BTC holders to mint tBTC for use on Ethereum and redeem tBTC on Ethereum for BTC on the Bitcoin network.

Since its launch, tBTC has grown their TVL to $217.1M according to Threshold’s tBTC Dune dashboard. While decentralized assets are the preferred choice for additions to the Capital Pool, the current TVL presents a ceiling for future growth in the Mutual’s BTC-based lines of business, where cbBTC is showing clear signs of growth that will likely pass the tBTC TVL within the next month, if not sooner.

At this time, tBTC doesn’t present the Mutual with a scalable BTC derivative.

Specification

If members were to vote in favor of onboarding cbBTC to the Capital Pool, the Advisory Board would onboard cbBTC as an asset in the Capital Pool and configure the [whatever the parameter here that determines the minimum amount we need vs. the max we can hold without going back to governance].

Once that step is complete, the Advisory Board would work with the Foundation Engineering team to swap ETH for $1M worth of cbBTC. The Advisory Board would then work with the Foundation Engineering team to enable cbBTC-denominated cover buys at user interface (UI) level to complete the onboarding process.

Proposal Status

This RFC was open for review from 24 September until 8 October. No substantial comments were received, and the feedback during the review period was overall positive. As such, the RFC transitioned to an NMPIP.

The NMPIP will be open for review from 8 October until 16 October. After this review period, the NMPIP will move to an onchain vote on Thursday, 17 October.

NMPIP 239 is open for voting from 17 October at 3pm UTC until 20 October at 3pm UTC.