We wanted to clarify that the claim is for $47,150.79 following a severe and sudden economic event in ExtraFi’s OVN lending pool. The loss was computed as $55,623.79, the value of the position on ExtraFi on October 10th, minus $5,991.37, the residual value after the incident when stabilization occurred.

The claimant views the root cause of the loss as a governance-level disruption due to abrupt tokenomics changes implemented by the OVN protocol team. These changes, outlined by OVN’s CEO in public communications, altered core protocol mechanisms, resulting in a liquidity crisis and forced mass liquidations. So the view is that the loss-inducing incident was not a market-driven event, but an unexpected structural shift outside of normal protocol operations. The governance action, akin to a malicious protocol upgrade, destabilized the OVN lending pool, constituting a “Sudden and Severe Economic Event” under clause 1.1.2 of Nexus Mutual’s cover terms.

Supporting Evidence:

Governance Disruption: The protocol’s direct policy changes triggered significant liquidity contractions, removing liquidity incentives without community input, similar to a forced governance takeover.

Systemic Impact beyond market movements: The tokenomics adjustments caused a protocol-wide severe liquidity event, making liquidation cascades inevitable, akin to oracle manipulation. These changes were acknowledged as unforeseen by the protocol’s leadership.

Policy Reference:

Clause 3.5 of the cover terms specifies that losses from asset price movements are excluded unless the price movement meets the definition of oracle manipulation per clause 1.1.2. The OVN token’s price decline resulted from governance-level adjustments—not market speculation—triggering liquidation thresholds en masse, akin to oracle manipulation through internal systemic policy failure.

As no votes were cast on claim 23: Nexus Mutual the claimant has asked to have the claim reconsidered in light of the above.

The evidence provided did not meet the criteria in the Protocol Cover wording to validate a loss of funds due to one of the covered terms for ExtraFi Protocol Cover.

The change in tokenomics was an offchain decision to reduce incentives on Aerodrome for the OVN liquidity pool. This decision was made by the Overnight team, who provided bribes from their foundation’s funds. This is not related in any way to the ExtraFi protocol.

A reduction of liquidity in an Aerodrome pool does not constitute oracle manipulation.

Most importantly, no funds were lost according to the onchain evidence. The claimant withdrew more OVN than they originally deposited into ExtraFi, which is evidence that they earned interest on their OVN while it was deposited into the ExtraFi protocol. They did not suffer a loss of funds due to bad debt, oracle manipulation, or a governance attack, nor did they suffer a loss of funds due to a lack.

The claimant was able to swap their OVN for USDC after they withdrew from the ExtraFi protocol as I noted in my assessment.

Protocol Cover does not protect against a loss of value. For that, a user would need to use options or hedge with a short position—both are financial instruments available in other DeFi protocols.

When Claim Assessors believe a claim should be denied, they do not need to cast votes. Assessors only cast votes if they believe a claim is valid, and other Assessors who believe a claim should be denied can vote to deny a claim only after someone has voted to approve a claim. This is how the Nexus Mutual protocol is designed to work. This ensures that repeated claim submissions do not require Assessors to spend ETH on gas costs to deny invalid claim submissions.

The window for filing a claim is either during the active cover period or up to 35 days after the active cover period ends. This claim expired on 9 November 2024. The claim and any appeals could have been filed by 14 December 2024–the last day of the grace period. No subsequent claim requests can be filed for this cover.

This is despite the fact that the original cover was purchased after the stated loss event occurred and despite the fact that the claim was filed 65 days after the stated loss event occurred on 9 October 2024. While there is a 14-day cool-down period between when a loss event occurs and when a claim can be filed, the claimant waited an extra 51 days beyond the cool-down period to file their claim.

I hope this provides clarity on why this claim cannot be appealed and why it is not a valid claim request due to the nature of the stated loss of value in the original claim submission.

To the Nexus Mutual Assessors and Governance Community:

Addressing Timing of the Loss Event

The cover policy became effective October 10th, 2024, at 01:01:13 AM UTC; also viewed as October 9th when viewing in PST, but for on-chain coverage, UTC is the standard reference.

The actual financial loss was only finalized once liquidation transactions occurred during my coverage period; this was a multi-day liquidation cascade rather than a single discrete event.

Therefore, the critical ‘Loss Event’—the point at which my positions were closed and I suffered a net shortfall—took place on-chain after my policy took effect.

The claim was filed using Nexus’ on-chain claim submission form and was open for voting, indicating it was accepted by the system as timely filed. OpenCover confirmed the claim was submitted on December 13, and the Nexus Mutual claims portal shows the assessment period of 12/13/2024 – 12/16/2024.

Under the 30-Day Cover scenario, which ran from October 10, 2024 (01:01 UTC) to November 9, 2024 (01:01 UTC), the latest claim filing date would be December 14, 2024 (35 days after November 9).

Because the claim was submitted by December 13, 2024, this is within the permissible window.

“Under a fair reading of the cover terms (including Clause 1.1 and the exclusion at Clause 3.4.1), coverage should apply if the actual loss of funds was conclusively realized after the policy start date—consistent with standard insurance principles, especially in continuous or multi-phase DeFi events.”

My insurance coverage was purchased in USDC terms, and I suffered a significant reduction in the USDC value of my position.

From a user perspective, OVN lending was presented as a core feature of the ExtraFi platform. The ExtraFi interface, documentation, and marketing materials explicitly promoted depositing OVN to earn yield. This co-marketing suggested OVN was not an unrelated, external asset, but rather an integral part in the ExtraFi ecosystem.

ExtraFi’s code and lending architecture relied on OVN markets for users to borrow, lend, and earn interest. If OVN had not been integral, ExtraFi would not have prominently featured OVN-lending as part of its main product line.

Overnight (the team behind OVN) may be nominally distinct, but ExtraFi’s functionality and liquidation events were directly impacted by OVN’s tokenomics. Abrupt changes to OVN’s liquidity or incentives caused a cascading liquidation that severely affected user positions within ExtraFi.

Moreover, ExtraFi had the ability to set parameters for OVN lending, suggesting a partnership or integrated mechanism, not just an external plugin. Users were encouraged to deposit OVN through ExtraFi, making OVN-lending a “key ExtraFi product.”

Denying the claim on grounds that ExtraFi itself was not the source of the issue overlooks the interconnected nature of these protocols. If ExtraFi’s architecture and user-facing services depend on OVN, then OVN’s governance-level changes constitute a material part of ExtraFi’s operation.

USDC-Denominated Coverage Implies Protection of Capital Value.

The cover policy explicitly references a Cover Amount in USDC and a Deductible denominated as a percentage of that USDC amount.

If the policy were purely about returning the same quantity of tokens (regardless of price), there would be little reason to denominate coverage in a stable asset. This structure implies coverage is intended to protect against an economic loss in stablecoin terms;

“funds” typically refer to the real economic or stablecoin value—particularly when the premium and coverage are denominated in USDC.

Clause 3.5 excludes ordinary market price fluctuations but allows coverage if the price movement meets the definition of a Sudden and Severe Economic Event under Clause 1.1.2 (e.g., malicious governance takeovers, severe protocol failures).

The “abrupt tokenomics changes” behind OVN/ExtraFi, acting like a forced governance disruption, were not normal market volatility or mere speculation. They triggered liquidation thresholds in a manner resembling a malicious or extreme governance action, causing sudden, systemic impact.

A reasonable user buying coverage in USDC would expect that depositing stablecoin-equivalent capital—and later receiving significantly less stablecoin value—constitutes a loss of funds if it arose from a protocol-level failure or governance breakdown.

If Nexus Mutual intended to cover only numeric shortfalls in token quantity (ignoring stablecoin value), referencing USDC would be misleading. Under good faith and contra proferentem principles, any ambiguity should favor the insured, protecting the stablecoin value.

There are no specific policy sections that definitively exclude OVN or disclaim coverage solely for token quantity. Given the integrated nature of OVN within ExtraFi and the policy’s USDC denomination, the claim should be recognized as valid.

This interpretation aligns with users’ reasonable expectations and the broader spirit of the policy, ensuring that genuine economic losses caused by extraordinary protocol actions are covered.

Cover ID 1375 was finalized onchain on 10 October 2024 at 10:44:35 AM UTC. The first OVN liquidation occurred on 10 October 2024 at 02:44:41 AM +UTC. There’s a full Dune dashboard that tracks all of the OVN liquidations on ExtraFi here.

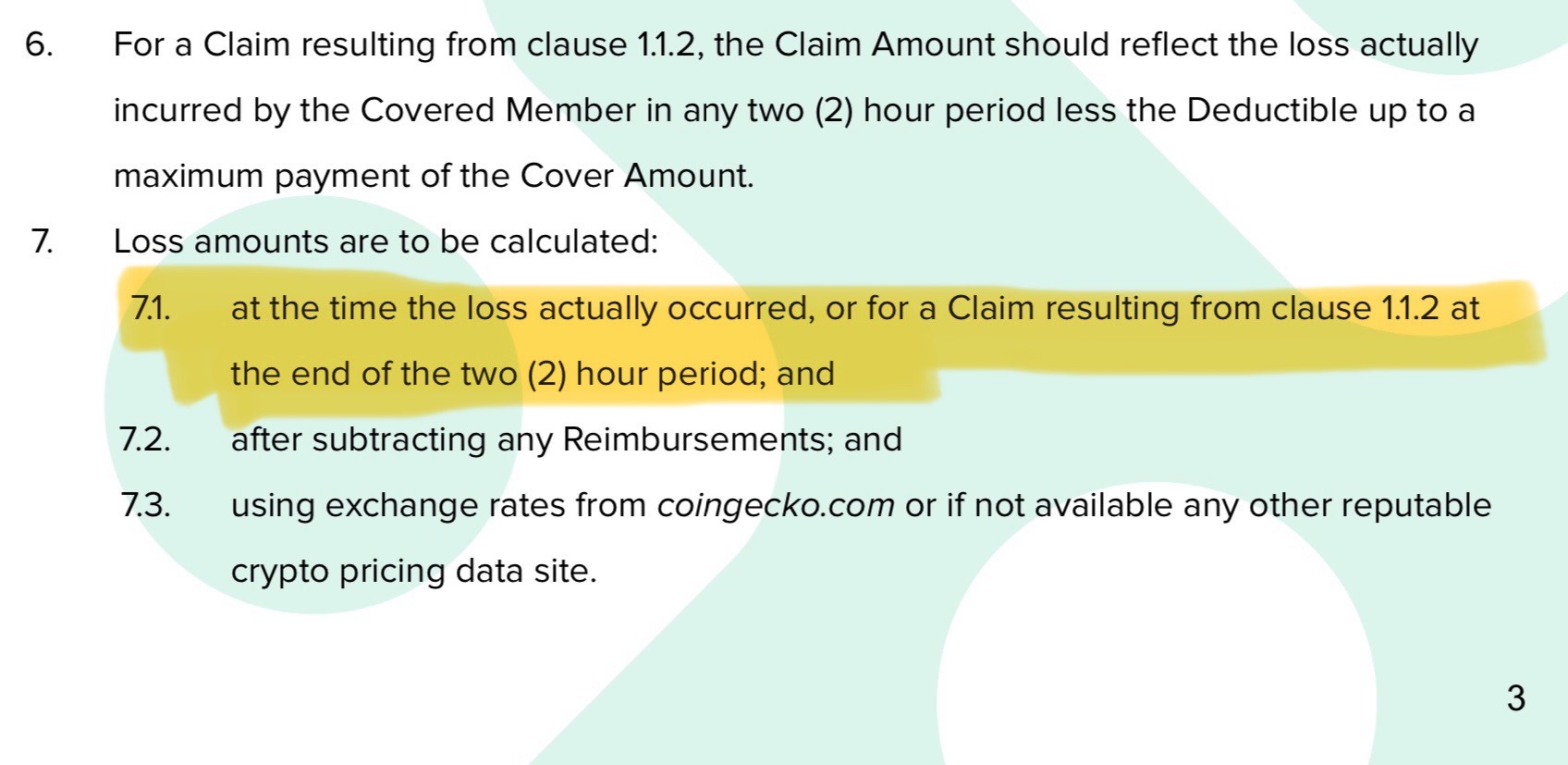

According to Clause 7.1, losses would be limited to the end of the two (2) hour window when the loss event began.

The loss event you’re claiming for does not qualify as valid, per the Protocol Cover wording. The liquidation cascade was not due to oracle manipulation or a governance attack. No evidence has been provided that substantiates either of these claims.

ExtraFi is a leverage protocol that allows users to lend their assets, which are borrowed by leverage traders who take on leveraged exposure to generate additional yield. If those leverage traders have their positions liquidated, their positions will be unwound and sold to cover their debt. The remaining funds will be returned to those leverage traders less any liquidation penalties. Liquidations large or small are a normal occurrence within a leverage or lending protocol. The ExtraFi protocol behaved as intended and no loss of funds occurred, as no bad debt was created.

The causes of loss you alleged regarding oracle manipulation and governance attacks are unsubstantiated.

You suffered a loss of value, not a loss of funds, as I noted in my summary of your claim submission. You were able to withdraw your original OVN deposits plus the interest you earned and you subsequently sold your OVN for USDC. You did not suffer a loss of funds. If you did, you would have withdrawn less OVN than the original amount you deposited.

Your cover demination has no bearing on the underlying coverage. The cover denomination only specifies what asset you would be paid out if you were to you suffer a valid loss of funds and if your claim were approved by Claim Assessors.

Nexus Mutual Protocol Cover is not a put option you can exercise on a token’s value dropping. It will protect you against a loss of funds due to one of the covered terms.

Subject to clause 3 (Exclusions), Claim Assessors may approve a Claim made under this Protocol Cover if:

1.1 the Covered Member is a user of the Designated Protocol and during the Cover Period the Designated Protocol loses Covered Member funds in excess of the Deductible as a direct result of the Designated Protocol failing from either:

Emphasis mine

The cover wording clearly states a Covered Member must suffer a loss of funds. There is no mention anywhere about a loss of value being covered and there’s no language that states the cover denomination gives a Cover Member the right to claim for a loss of value.

The Overnight team’s decision to reduce bribes on their Aerodrome pools does not constitute a governance attack, as no governance vote was held on the matter. This decision did not include any changes to any onchain contracts.

Governance takeovers are defined in the Protocol Cover wording as:

governance takeovers where a malicious actor forces through a malicious

upgrade to a Designated Protocol smart contract.

No such change was made. There has been no proof provided that shows evidence of any onchain contracts being modified through a governance proposal, nor was there evidence provided that showed any malicious proposal was put forward in onchain governance.

You had the option to purchase ExtraFi Protocol Cover in either USDC or ETH denomination. You chose USDC. Your decision to denominate your cover in USDC does not alter the protections provided by the underlying Protocol Cover wording.

OVN is not a stablecoin, as I have stated above, and there’s no mention of Protocol Cover protecting a Covered Member against a loss of value anywhere in the cover wording.

I have voted to approve many, many claims in the past. Where a loss of funds meets the terms outlined in Nexus Mutual’s cover wording documents, I’m happy to approve and pay a claim.

Unfortunately, this loss event did not meet the terms outlined in the Protocol Cover wording.

If this loss event were to meet the terms in the Protocol Cover wording, you still would not have been eligible because the cover in question was purchased nearly 8 hours after the stated loss event began and 6 hours after the two-hour window would have closed according to Clause 7.1 in the Protocol Cover wording.

Because the grace period has passed for Cover ID 1375, no further claims can be filed onchain and no additional appeals can be made for this Cover ID.

“I acknowledge that you view the first liquidation (2:44 AM) as the moment the ‘loss event’ began, but my position was not liquidated until after 10:44 AM, when my coverage was active. I believe the multi-day liquidation wave triggered by OVN’s abrupt tokenomics changes should not be treated as a single event starting at 2:44 AM, especially since the crucial forced liquidation impacting me occurred later.

Furthermore, while I understand your interpretation that no on-chain governance proposal was maliciously executed, I submit that OVN’s unilateral off-chain decision to remove incentives from Aerodrome amounts to a forced governance disruption across the broader ExtraFi–OVN ecosystem—akin to a Clause 1.1.2 event.

While I respect your input and time to evaluate this claim - I hope these points are considered for improvements and wider protocol coverage as these events should have risk coverage.

“I also want to note that Open Cover themselves recognized a shortfall in coverage for multi-composed protocols. In one of their early responses to me, they stated:

‘We are about to release a cover product that gives you “all in one” cover on multiple composed protocols to make it more straightforward to get covered in setups where users leverage composed protocols.’

This acknowledgment suggests that the current coverage framework—focused on a single “Designated Protocol”—may not adequately protect users who interact with multiple, interdependent DeFi platforms. My situation illustrates precisely that gap, as Overnight’s tokenomics changes within Aerodrome materially impacted my ExtraFi position. If the coverage had explicitly accounted for such interconnected risks, I believe my claim would have been valid.

The forthcoming “all in one” cover indicates that both Open Cover and Nexus Mutual see the need for more integrated coverage solutions. I respectfully urge further clarity and consideration in existing policy wordings for scenarios like mine, where off-chain decisions in a related protocol create a sudden cascade in the covered protocol. Ensuring that such events qualify as covered losses would better align with user expectations and the evolving realities of DeFi composability.”

This claim is for $47,150.79 following a severe and sudden economic event on ExtraFi’s OVN lending pool. The loss was computed as $55,623.79, the value of the position on ExtraFi on October 9th before the incident, minus $5,991.37, the value of the position after the incident when residual value stabilized.

There is no onchain evidence that you had a leverage position that was liquidated. As you stated in you original claim submission and in the statement above (“We wanted to clarify that the claim is for $47,150.79 following a severe and sudden economic event in ExtraFi’s OVN lending pool.”), you deposited OVN in the ExtraFi lending pool and suffered a loss of value, not a loss of funds. As I noted previously, you did not suffer a loss of funds and even if your ExtraFi coverage included Overnight or Aerodrome, this would not have been a covered event, as no loss of funds occurred in any of these three protocols.

A change in incentives decided by the Overnight team does not constitute a malicious governance proposal that changed the protocol’s smart contracts.

“Sudden and Severe Economic Event” is defined in the cover wording as:

be clearly outside the normal or intended operation of the Designated Protocol; and

Liquidations within a lending and leverage farming protocol are expected if positions drop below their respective health factors. No issues occurred during the liquidation process within the ExtraFi protocol.

be caused by either:

oracle manipulation or failure; or

No evidence or oracle manipulation has been provided, and there’s no onchain record that any oracle manipulation occurred. A reduction in liquidity incentives does not constitute oracle manipulation.

severe liquidation failures where liquidation processes of the Designated Protocol clearly fail to operate correctly; or

Liquidations occurred as expected on ExtraFi and no bad debt occurred within the lending markets, as evidenced by the fact that you were able to withdraw your principal plus the interest you earned as a lending in the ExtraFi lending pool.

governance takeovers where a malicious actor forces through a malicious

upgrade to a Designated Protocol smart contract.

No malicious upgrade to the protocol occurred. A change in liquidity incentives do not consitute a governance takeover. The wording is clear about this.

We have offered Bundled Protocol Cover since Spring 2024, and we have been building upon that cover product to provide protection across multiple protocols in one Cover NFT. We’ve been focused on making it easier to protect against a loss of funds in DeFi. I agree that we can offer comprehensive cover that extends beyond just one (1) protocol to better protect users.

However, all of our bundled cover products protect against a loss of funds and not a loss of value.

If you were to use a deriviative protocol to take a short position on OVN to hedge against downside price movements, you would have been able to protect against a drop in OVN price.

As I stated previously, Nexus Mutual’s cover products are not designed to act as a put option for crypto assets deposited in DeFi protocols. If you were to have just held OVN in your wallet, you still would have suffered a loss of value. The loss of value was not due to any hack or exploit.

I want to be very clear that even if you had purchased a Base DeFi Pass, this would not have been a covered event. The type of coverage had no bearing on the validity of this claim.

I won’t respond beyond this comment, as I believe I’m repeating points I’ve made previously in other comments between the this and the previous forum post.