Summary

The Investment Committee proposes a framework for keeping a minimum amount of “cash” assets in the Capital Pool, totalling 1m DAI and 12,500 ETH. These consist of:

- 1m DAI and 500 ETH to be used as immediate liquidity for claim payments

- 9,000 ETH as liquidity for the RAMM

- 3,000 ETH to be used as emergency collateral for the USDC loan associated with the Cover Re deal.

We propose delegating the ability to convert stETH and rETH back to ETH in the Capital Pool to the Investment Committee, aided by the Advisory Board in technical implementation, in order to maintain the minimum amount of “cash” assets as described above. The Investment Committee will, only if necessary to meet the minimum cash assets, perform the following actions, in order.

- Reduce the stETH in the pool to the same amount as the rETH in the pool.

- Reduce the stETH and rETH to 15% each as a proportion of the Capital Pool.

Introduction & Rationale

The purpose of this proposal by the Investment Committee is to outline the policy for:

- Maintaining a balance between the assets in the Capital Pool used for:

- paying for claims,

- providing liquidity to the RAMM, and

- investing the assets to generate a return

- Converting out of Nexus Mutual’s investment assets back to ETH in the short term.

The reasons for requiring this are as follows:

- ETH liquidity is required for ongoing redemptions from the RAMM

- A large portion of the existing ETH in the capital pool will be used to borrow USDC on Aave for the purpose of executing the Cover Re deal. All Cover Fees generated in stablecoins are best used to pay off the USDC loan. Some ETH will need to be set aside for topping up the collateral on the loan if required to avoid liquidation.

- Through investment gains and the redemptions from the Capital Pool, stETH has become a disproportionately large part of the assets.

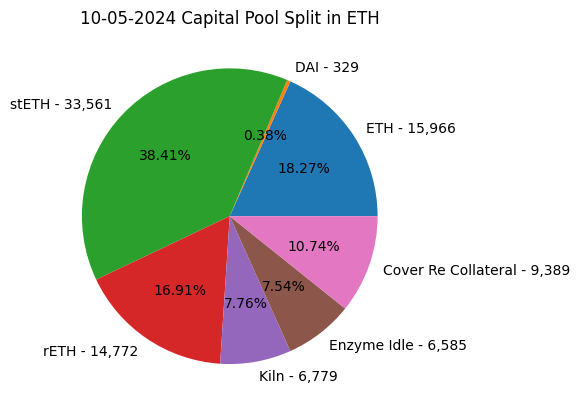

Current Projection of Pool Assets

The on-chain capital pool split, allowing for immediately known changes is as follows:

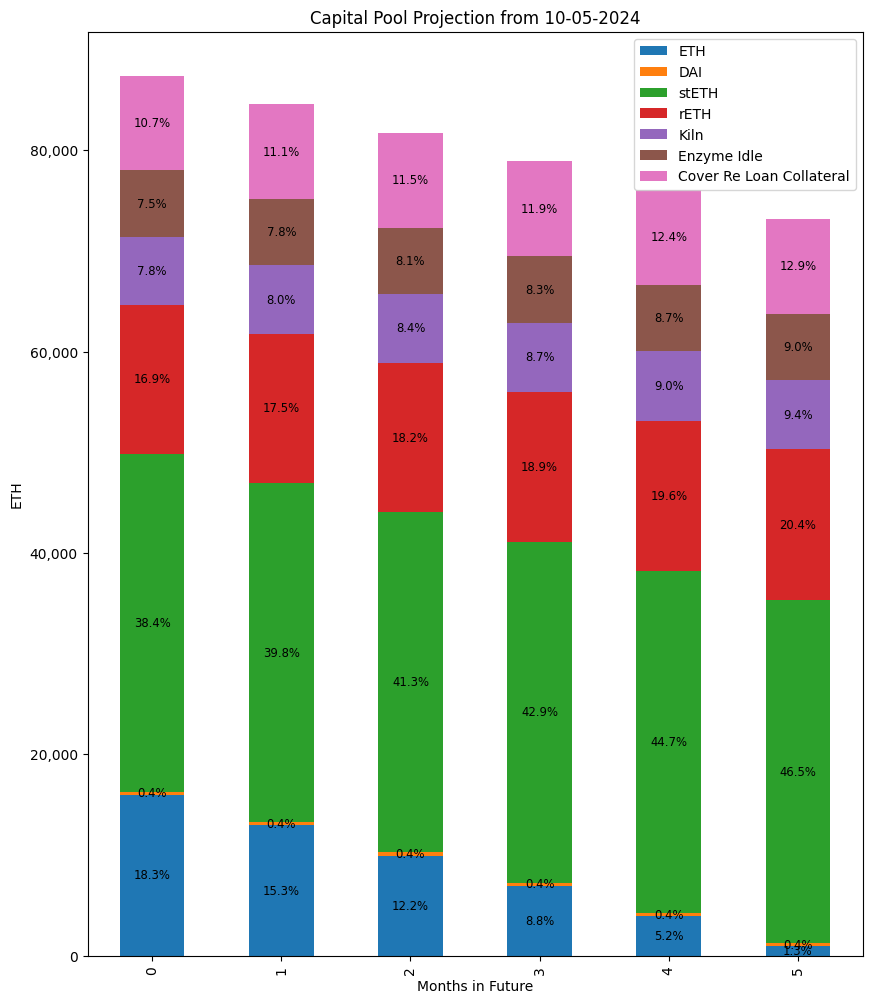

Based on the average changes in the Capital Pool since August ‘23, the following projections (source) can be made about the future progress of the Capital Pool:

Note that this allows for the Cover Re-related Aave USDC loan and associated collateral. We have also assumed a 70% claim ratio on all new incoming Cover Fees.

This shows the overexposure of the capital pool to stETH and the concern that ~4-5 months from now (around late September) the RAMM may be short of ETH liquidity if RAMM redemptions continue at the current rate of ~3,000 ETH / month.

Proposed Bucketing Framework

Assets Required for Claims

In the current state as at 10/05/2024, we have ~28,788 ETH of active cover, resulting in a cover-driven MCR of approximately ~6000 ETH. Of this, 62% is ETH based and 38% is DAI based

The Advisory Board has proposed to keep ~1m DAI aside on an ongoing basis to pay immediate claims after diverting the remainder of the stablecoins in the Capital Pool to invest in Cover Re.

Using the current ~60/40 split between ETH and DAI covers and an ETH/USD rate of $3000, the proportional amount to set aside for ETH claims is exactly 500 ETH (~$1.5m equivalent).

We therefore propose putting aside 1m DAI and 500 ETH ring-fenced for paying immediate claims.

This will mean we hold approximately 25% of the current cover-driven MCR in cash, with the rest being split up amongst RAMM liquidity and investment assets.

This should be revised if circumstances change materially in terms of:

- capital levels of the mutual,

- cover exposure,

- ETH prices

We suggest that the Investment Committee monitor and, if necessary, suggest adjustments to the amount ring-fenced for claims on an end-of-quarter basis.

RAMM

The RAMM mechanism is a way for members to mint and redeem their NXM in exchange for ETH. In order to allow redemptions of NXM, the mutual needs to have ETH available in the Capital Pool for this purpose.

The ability of members to exit the mutual when they choose should generally take priority over having assets invested.

We suggest ring-fencing a 3-month buffer of liquidity injection, which is replenished at minimum every 2 months.

At the time of writing (10/05/2024) we should aim to keep 9000 ETH in the capital pool allocated for member redemptions, representing the maximum possible liquidity that can be injected into the RAMM over three months.

At the start of each month, a check should be performed by members of the Investment Committee to ensure that there is 9000 ETH in the capital pool ring fenced to be used as liquidity injection into the RAMM if required.

If that is not the case, some investment assets should be converted into ETH so that there is sufficient liquidity.

Investment Assets

Any assets that aren’t required to immediately back claims or ring fenced as potential liquidity injections into the RAMM can be used as investment assets.

As at 10/05/2024, this would imply that of the approximately 87.05k ETH worth of non-stablecoin assets in the Capital Pool, 77.55k ETH can be used in investments.

61,680 ETH is already split between stETH, rETH and the Nexus Mutual Treasury Yield Enzyme vault, with another 9,390 ETH expected to be invested as collateral for the Cover Re deal. We also propose that 3,000 ETH is set aside as emergency additional collateral for the Cover Re Aave v3 loan.

This leaves 3,480 ETH which could at this time be used to generate additional yield via the normal governance process for making investments from the Capital Pool.

Given the size of this amount and the current rate of RAMM redemptions, we do not recommend that this remaining amount is used for investments.

However, we would still encourage members to utilise the idle WETH in Nexus Mutual’s Enzyme vault in order to generate returns.

Exposure to Investment Assets

An important consideration is the distribution of investment assets as we require more liquidity for the RAMM.

By the above recommendations, this leaves:

- 1m DAI (or ~333 ETH) and another 500 ETH as the cash allocation for claims,

- 9,000 ETH set aside as liquidity for the RAMM and

- 3,000 ETH as emergency collateral for the Cover Re loan,

totalling 12,833 ETH-equivalent retained in the Pool in “cash” assets.

At the current rate of redemptions, we expect this threshold to require topping up in about 2 months, roughly by the end of July ‘24.

The percentage totals in 2 months time are projected to be as follows:

| Asset | Projected Percentage of Capital Pool on 10/07/2024 | Risk Category |

|---|---|---|

| stETH | 41.3% | High |

| rETH | 18.2% | Low |

| Enzyme - Kiln | 8.4% | Low |

| Enzyme - Idle | 8.1% | Low |

Mainly, there is a concern regarding the extremely high exposure to stETH/Lido which has moved into the high risk bucket as per the Investment Philosophy.

Even though there are arguments to be made regarding the systemic importance of Lido to the Ethereum ecosystem providing some risk mitigation, we feel that the best approach is to diversify our exposure both to reduce concentration risk and to contribute to the broader diversification of Ethereum’s security model.

Proposal

We propose giving members of the Investment Committee, aided by the Advisory Board, the power to make the following adjustments as the Capital Pool develops in line with the above Bucketing Framework:

In order to meet the requirements of holding ETH for claims and RAMM liquidity:

- If required, reduce our exposure to stETH to the same percentage level of the Capital Pool as rETH.

- If required, reduce both stETH and rETH investments to 15% each as a proportion of the Capital Pool.

The above approaches are consistent with keeping a diversified pool of investments, with each individual investment kept below 20% of the entire capital pool as per the Investment Philosophy

Because of uncertainty surrounding the development of the Capital Pool, these steps are to be taken gradually, as ETH is required for the Claims and RAMM buckets, rather than all at once. Divestment actions are generally to be taken after the 12,500 ETH and 1,000,000 DAI cash asset threshold has been breached, finding a balance between optimal bucketing according to the above framework and the operational overhead associated with asset conversions in the Capital Pool.

We expect the first of the current stETH investment to be converted back to ETH at the end of July.

We also propose that if circumstances change (e.g. RAMM withdrawals from the Below Pool slow down or activity shifts into the Above Pool), the members of the Mutual allow the Investment Committee to not follow through on the above actions if the Committee determines that they are not required.

Proposal Status

Open for review and comment for 12 days until Monday 3 June.

After incorporating any feedback, this RFC will transition to an NMPIP.