Summary

This proposal recommends onboarding Threshold Network’s tBTC as a Capital Pool asset for Nexus Mutual. Integrating tBTC offers a strategic opportunity to enhance the safety and resilience of the Capital Pool by diversifying beyond the current cbBTC, which, while advantageous in its own right, relies on centralized custody and introduces potential points of attention. In contrast, tBTC—fully backed one-to-one by native Bitcoin—brings a unique combination of permissionless access, robust decentralization, and cutting-edge security that aligns seamlessly with Nexus Mutual’s trustless ethos.

Unlike cbBTC, tBTC operates as a fully permissionless system, enabling anyone to mint or redeem it without intermediaries or gatekeepers. Built on the Threshold Network, tBTC decentralizes custody across a rotating group of independent node operators, eliminating single points of failure and mirroring Nexus Mutual’s community-driven governance model.

The security of tBTC is further reinforced by threshold cryptography, requiring a majority consensus among operators (e.g., 51 out of 100) to manage the underlying Bitcoin via a multisig-like mechanism. By adopting tBTC, Nexus Mutual not only diversifies its Capital Pool with a premier store of value but also strengthens its foundation with an asset that embodies decentralization and resilience.

- Stage 1: Onboard tBTC as an asset in the Capital Pool

- Stage 2: Swap part of cbBTC to tBTC (initial amount of 25%)

- Stage 3: Swap part of cbBTC to tBTC (second amount of 25% reaching 50%)

- Stage 4: Swap ETH for tBTC (amount of $500k – half of NMIPIP 239 proposed)

Motivation/Background

tBTC is Threshold’s decentralized and permissionless bridge that brings BTC to Ethereum, Arbitrum, Base, Polygon, Optimism, Solana and other chains. Users wishing to utilize their Bitcoin on Ethereum and other chains can use the tBTC decentralized bridge to deposit their native Bitcoin into the system and get a minted tBTC token in their EVM wallet.

tBTC enables users to have access a bridged Bitcoin, which can be permissionlessly minted and redeemed, where the BTC that backs it is not held by a central intermediary, but is instead held by a decentralized network of nodes using threshold cryptography. This implies a fully decentralized and permissionless experience for BTC.

tBTC is present on other markets such as AAVE Ethereum and Arbitrum market and following its approval, tBTC’s initial supply cap was reached within 72 hours, prompting an increase to meet the overwhelming demand. This rapid adoption underscores the market’s appetite for trust-minimized BTC solutions in DeFi. It is also available on Compound platform.

tBTC on Ethereum has a current supply of 4.252 BTC worth $336M at current price.

Benefits for Nexus Mutual

- Further decentralization and trust minimization for Nexus Mutual funds.

- A range of options for those who wish to diversify on a decentralized option of wrapped BTC.

- High User Demand, since its initial deployment on Aave’s Ethereum market, tBTC reached its initial 500 BTC supply cap within the first week. The cap has been increased multiple times, now sitting at 2200 BTC, highlighting strong user interest.

- Preferable yields on tBTC through active incentive participation, boosting Venus protocol use and TVL.

Rationale for onboard tBTC

On NMPIP 239, Nexus Mutual onboarded cbBTC as a Capital Pool asset, a preferable choice over other options—especially WBTC—due to concerns stemming from BitGo’s August announcement and subsequent ownership changes. Although no issues have arisen since then, it remains premature to fully trust cbBTC as a Capital Pool asset given uncertainties about its management and the potential ripple effects of its significant market cap. While cbBTC is centralized and managed by a single entity, Coinbase has demonstrated a strong reputation in custody, serving both itself and third parties, including Strategy and several ETFs. Additionally, Coinbase recently published its Proof of Reserves for cbBTC, a positive step toward transparency.

However, despite this effort to minimize trust concerns, the centralized nature of cbBTC remains a factor to consider. It is prudent for Nexus Mutual to diversify its funds into secure, fully decentralized alternatives like tBTC. This approach ensures that institutional shifts, mismanagement, hacks, or even government interventions cannot compromise or seize Nexus Mutual’s funds, which are custodied on-chain, including the native Bitcoin backing tBTC. The Threshold Network publicly lists all wallets holding the Bitcoin that backs tBTC accessible at tBTC v2 Systems - Decentralized Bitcoin on Ethereum and every tBTC can be redeemed for BTC at any time, permissionlessly, without reliance on a centralized institution.

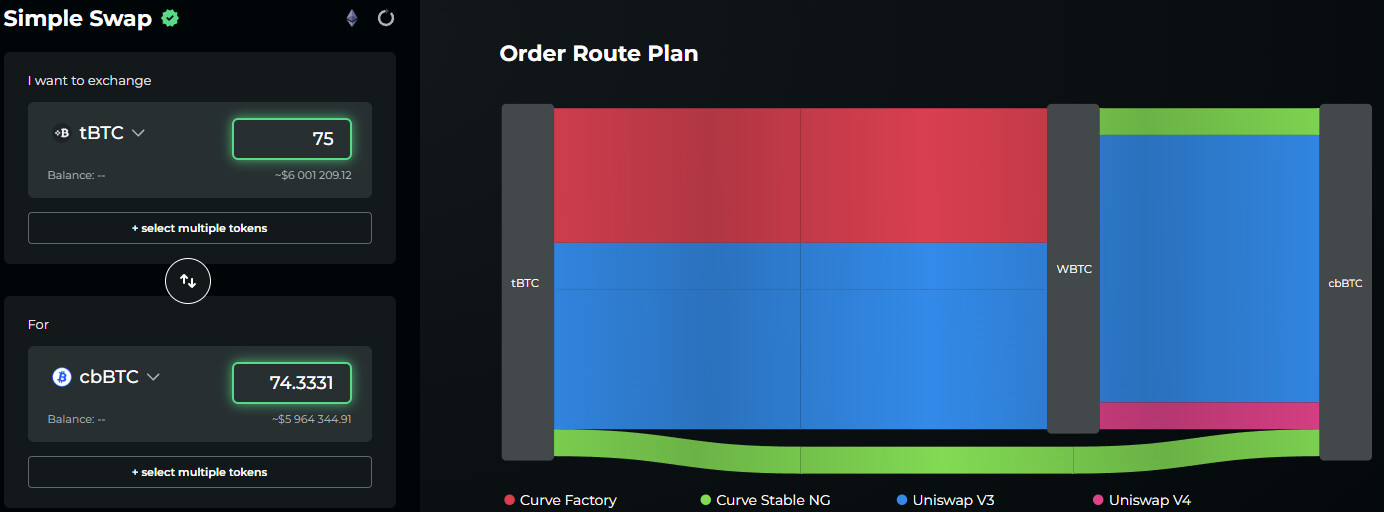

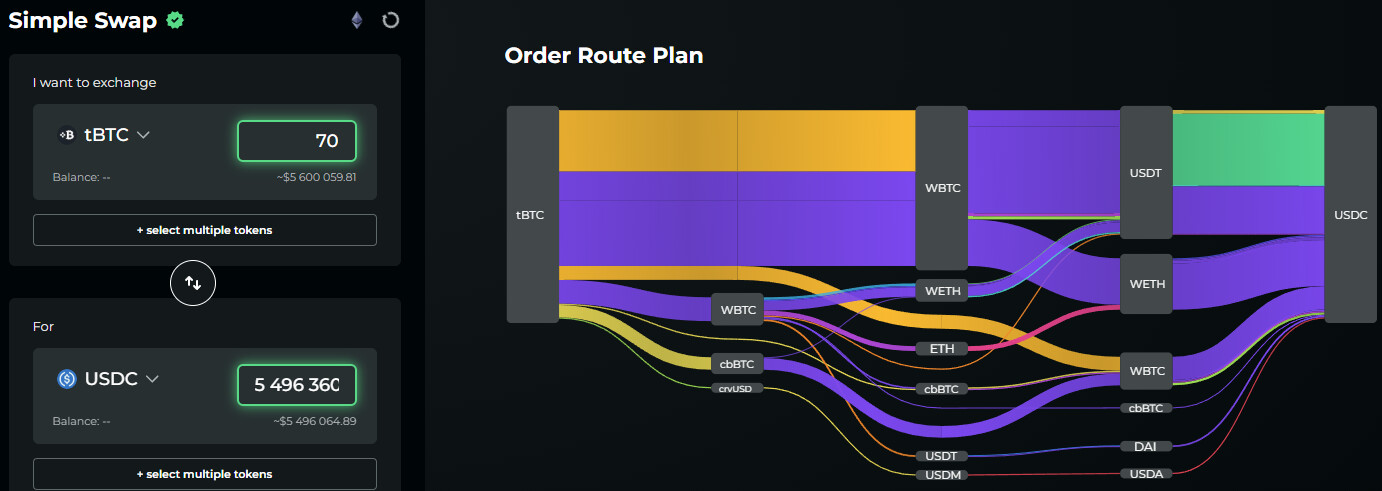

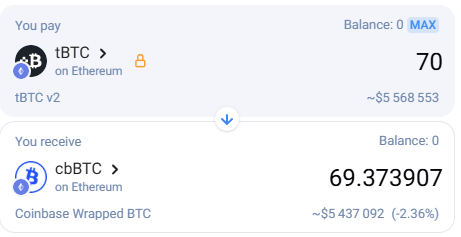

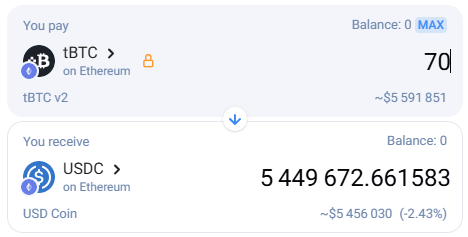

Migrating a portion of current cbBTC holdings to tBTC preserves value while enhancing trust in Nexus Mutual’s funds, reducing long-term risk. We propose that Nexus Mutual exchange 50% of its current cbBTC holdings for tBTC, with the transition executed gradually by the Advisory Board, beginning with an initial shift of 25%.

I also propose grant the Advisory Board the power to conduct the swap of ETH for tBTC (initial amount of $500k) half of what initially proposed for cbBTC on NMIP 239.

tBTC Liquidity and Market Risk Assessment

tBTC has current a supply of 4,252 BTC worth $366M at Ethereum ecosystem and is present on several DEXes, Lending and Yield platforms which have a fair amount of liquidity provided and interesting options for liquidity providers, lenders and borrowers which allows Nexus Mutual to swap it for whatever other main asset needed.

Moreover, tBTC can always be redeemed 1:1 for Bitcoin permissionlessly, ensuring flexibility and trustless access to native BTC at any time.

More can be found at https://defillama.com/yields?token=TBTC

Dashboard on Decentralized LP liquidity: https://dune.com/sensecapital/tbtc-liquidity

List of main DEXes where tBTC is listed and its approximate pool TVL

UniSwap - $8.64M in USD

Curve - $21.10M in USD

Aerodrome - $6.38M in USD

Velodrome - $3.34M in USD

Balancer - $1.1M in USD

PanckakeSwap - $60,242 in USD

List of main Lending and Yield Platforms where tBTC is listed and its approximate supply

AAVE - $77.50M in USD

Compound - $26.12M in USD

Morpho - $5.75M in USD

Merkl - $5.75M in USD

Convex Finance - $7.21M in USD

List of main Risk Assessments by independent services

AAVE Onboard of tBTC for Arbitrum market made by LlamaRisk (Feb, 2025)

AAVE Onbaord of tBTC for Arbitrum market made by ChaosLabs (Feb, 2025)

Venus Onboard of tBTC for Ethereum market made by ChaosLabs (Feb, 2025)

Compound Onboard of tBTC for Ethereum market made by Gauntlet (Jul, 2024)

AAVE Onboard of tBTC for Ethereum market made by ChaosLabs (May, 2024)

AAVE Onboard of tBTC for Ethereum market made by LlamaRisk (May, 2024)

Collateral Risk Assessment: Threshold BTC (tBTC) made by Llama Risk (Dec, 6th 2023)

Liquidity simulation with no significant price impact

Odos

1Inch

Specification

Ticker: tBTC

Contract Address:

Ethereum: 0x18084fbA666a33d37592fA2633fD49a74DD93a88

Useful Links:

Project: https://www.threshold.network/

Minting Dashboard: https://dashboard.threshold.network/tBTC/mint

Bridge to other Chains: Portal tBTC Bridge

GitHub: GitHub - keep-network/tbtc-v2: Trustlessly tokenized Bitcoin everywhere, version 2

Docs: tBTC Bitcoin Bridge | Threshold Docs

Audit: About

Immunfi Bug Bounty: https://immunefi.com/bounty/thresholdnetwork/

Llama Risk Report: Collateral Risk Assessment: Threshold BTC (tBTC) - HackMD

Twitter: https://twitter.com/thetnetwork

Discord: Threshold Network ✜

Dune: https://dune.com/threshold/tbtc

https://dune.com/sensecapital/tbtc-liquidity

Extra information about tBTC

Emission schedule

tBTC is one-to-one backed with real Bitcoin, meaning that there isn’t an emissions schedule, but a mint and redeem function that adjusts the supply of tBTC based on native BTC coming into and out of the system.

High-level overview of the project and the token.

tBTC is a decentralized wrapped Bitcoin that is 1:1 backed by native BTC. Unlike other wrapped Bitcoins, the BTC that backs tBTC is not held by a central intermediary, but is instead held by a decentralized network of nodes using threshold cryptography.

tBTC is trust minimized and redeemable for native BTC without a centralized custodian. It can be used across the entire DeFi ecosystem.

tBTC can be used as collateral, liquidity, a store of value, and can be integrated with DeFi apps across all supported blockchains.

As with other BTC wrappers, tBTC provides cryptocurrency traders and general users with a BTC-pegged token that can be used to generate yield whilst holding native BTC.

History of the project and the different components: DAO and products.

tBTC v1 was launched in May 2020 as a decentralized Bitcoin bridge on Ethereum by an effort of contributors. It was developed initially by Keep Network in collaboration with Summa and was designed to use a system of bonded operators to secure BTC deposits via a random beacon and threshold cryptography.

tBTC v1 had an initial surge of interest, but its growth was limited due to architectural constraints. It was listed on Uniswap, Curve, and other DeFi platforms, competing with WBTC, renBTC, sBTC and others.

tBTC v2 was then created and developed under the Threshold Network DAO and aimed to fix tBTC v1’s limitations. It extensively utilises the Threshold Network’s threshold cryptography to create a secure BTC asset. tBTC is a product launched on Threshold Network, on which many other decentralized applications are being built.

Threshold Network DAO was born out of the first on-chain merger between two decentralized protocols, Keep Network and NuCypher early in 2022. The DAO has successfully operated since that time, and supports an active community of contributors that work towards building tBTC liquidity and usability.

How is tBTC currently used?

tBTC is used across a variety of chains and use cases. Some key utilities include Aave, Compound, GMX, EigenLayer, Synthetix, Morpho, Symbiotic, collateral asset for crvUSD, thUSD and solvBTC.

A comprehensible list can be found here:

https://defillama.com/yields?token=TBTC 4 & https://linktr.ee/earnyield

Token & Protocol) permissions (minting) and upgradability, multisig?and signers?

For tBTC, wallets are created periodically based on governance. In order for the wallet to move funds, it produces signatures using a Threshold Elliptic Curve Digital Signature Algorithm, requiring 51-of-100 Signers to cooperate. The 100 signers on each wallet are chosen with our Sortition Pool, and the randomness is provided by the Random Beacon. More can be found here - Wallet Generation | Threshold Docs

The Threshold Council multisig is a 6/9 Gnosis Safe multisig with 9 unique signers that form the Threshold Network Council. The Council has limited upgrade privileges over the smart contracts. However, those privileges do not include any custodial power over deposited BTC:

Council Multisig Ethereum Address: 0x9F6e831c8F8939DC0C830C6e492e7cEf4f9C2F5f

Social channels data (size of communities and activity)

Discord: 10,175

Twitter: 38,400

Github: 4,596 commits

Date of Deployment: August 2021

Number of transactions: 2.393.648 (across all chains)

Number of token holders: 15.918 (across all chains)

Observation

At this time it is not proposed to enable tBTC-denominated cover buys at user interface (UI) level, but opened to discussion.