Overview

The purpose of this proposal is to put forward an approach for repaying the Cover Re-associated Aave loan and increasing the collateral as ETH price drops to avoid liquidation.

We propose allowing the Advisory Board (“AB”), supported by the Foundation Engineering team to take the actions described below in respect of the current Aave V3 USDC loan without further governance approval.

The actions are:

- Repaying portions of the loan when excess stablecoins in the Capital Pool above the minimum cash threshold.

- Topping up the aEthWETH collateral using 3,000 ETH in the capital pool at each of the following ETH/USD price thresholds:

- $1600

- $1250

- $1000

- Executing an emergency repayment at the discretion of the Advisory Board if ETH/USD price drops below $500.

Background - Loan Details

The Aave v3 Ethereum supply & USDC borrowing markets were chosen by the AB as the lending markets best suited to the task because of the combination of deep liquidity, favourable liquidation parameters and proven resilience.

Chosen market: Aave V3 Mainnet

Original Borrowing Amount: USDC 6,201,996

Original Target Liquidation Price: $800/ETH

ETH Collateral: 9,340

The loan, alongside the 12m USDC investment into Cover Re was executed on 23/05/2024 using the AB Multisig.

Specification - Regular Repayment Approach

Amounts and Frequency

There is no reason to hold excess stablecoins within the Capital Pool unproductively instead of using them to repay the outstanding debt.

Therefore, Nexus Mutual should use any available stablecoins in the Capital Pool (in excess of a minimum threshold reserved for claims) to repay the loan and reduce both the overall interest accrued and the risk of liquidation. The minimum threshold of stablecoins to retain in the Capital Pool is proposed to be 1m USD equivalent.

Even for an amount as low as 10,000 USDC/DAI, the gas fees for

- sending stablecoins to the AB multi-sig used for the loan,

- swapping to USDC via CoW Swap if required,

- approving an amount of USDC to interact with the Aave contracts, and

- repaying a portion of the debt

typically add up to less than 1 month’s worth of interest on 10,000 USDC at the 6-month average borrowing rate of 8.78% (19/06/2024).

Any cash generated directly in the AB multisig, e.g., from the Cover Re investment or recoveries from previous stablecoin-denominated claims should also be used in the first instance to pay off the loan. These amounts are likely to be large enough to warrant an immediate transaction to pay off some of the debt.

To allow for the coordination time cost, we propose that whenever there is an excess of more than 50,000 USD-linked stablecoins in the Capital Pool above the minimum threshold, we use that amount to pay off the debt, with a maximum of one repayment transaction per month to avoid excessive admin. Smaller amounts are left at the discretion of the AB if persisting in the Capital Pool for a longer period.

Process for transfers from Capital Pool

The Capital Pool now contains both USDC and DAI. The target would be to hold the remaining 1m stablecoins in proportion to the USDC/DAI cover exposures. In practice we’d prefer to only transfer one currency at a time from the Capital Pool in order to save on gas fees.

Once there is at least 1.05m of USD-linked stablecoins in the Capital Pool, we propose the Advisory Board will initiate a request from the Capital Pool as follows:

-

The amount of stablecoins transferred for a repayment will be:

Amount Transferred = Total DAI + Total USDC in Capital Pool - 1,000,000

-

If only one of the DAI or USDC balances is sufficient to meet the Amount Transferred, then use that currency.

-

Otherwise transfer the currency which, after transfer, would result in the DAI/USDC ratio in the Capital Pool to be the closest to the ratio between Active Covers denominated in DAI and USDC.

Example 1:

Total DAI in Capital Pool = 1,049,000

Total USDC in Capital Pool = 6,000

Amount Transferred = 1,049,000 + 6,000 - 1,000,000 = 55,000

Currency to transfer: As there is insufficient USDC to meet the Amount Transferred, the AB will request that DAI is transferred to the AB Multisig.

Example 2:

Total DAI in Capital Pool = 550,000

Total USDC in Capital Pool = 600,000

Amount Transferred = 550,000 + 600,000 - 1,000,000 = 150,000

Active DAI Covers : Active USDC Covers = 50 : 50

Currency to transfer: Transferring 150,000 USDC will result in a 55:45 DAI:USDC split in the Capital Pool. Transferring 150,000 DAI will result in a 40:60 DAI:USDC split in the Capital Pool. As 55:45 is closer to the 50:50 Cover split, the AB will request that 150,000 USDC is transferred to the AB Multisig.

Nexus Mutual DAO’s Covers Dune dashboard should be used as the source of the required cover ratio.

Specification - Liquidation Policy

The Cover Re governance proposal suggested that the liquidation threshold used should equate to liquidation at a price of ~$800 per ETH.

We should not be actually liquidated under any circumstances, as the value of the collateral at the time of liquidation is greater than the value of the outstanding debt. For the Aave v3 Ethereum market, the value of the collateral is approximately 120% of the debt at the time of liquidation.

The chosen approach to prevent liquidation is to incrementally top up the collateral as ETH decreases in price in order to avoid selling ETH to pay off the loan at low ETH/USD prices.

| Strategy | Description | Pros | Cons |

|---|---|---|---|

| Increase the collateral | Use remaining funds in the Capital Pool to add to the collateral. Involves setting ETH price thresholds where the collateralisation ratio is deemed to be too low and bringing that ratio back up by increasing the size of the collateral. | De-risking gradually over time. Don’t have to sell ETH at any point at a price the community believes is unacceptable. | Requires availability of additional ETH in Capital Pool. Increases exposure to Aave every time the collateral is topped up. |

Collateral Top-ups

The suggested price thresholds for topping up the collateral are outlined below. When the ETH price drops below the price threshold, the additional collateral should be added to the position by transforming existing capital pool assets to additional aWETH in the multisig used for the loan.

The projections below have made the assumption that half a year has passed since the original loan with no repayments with the 6-month average ETH Supply and USDC borrow rates.

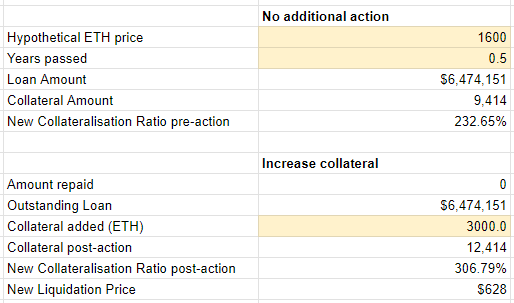

1. $1600

Amount of collateral to add: 3000 ETH

Outcome:

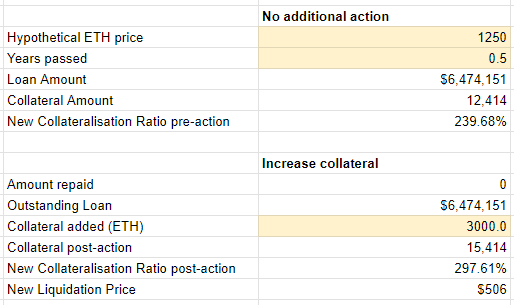

2. $1250

Amount of collateral to add: 3000 ETH

Outcome:

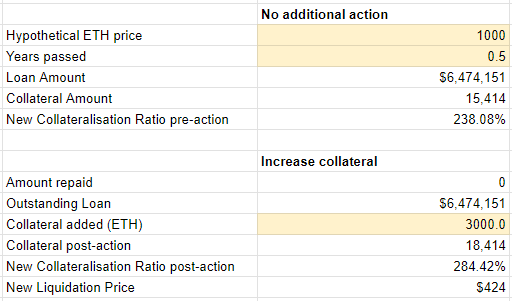

- $1000

Amount of collateral to add: 3000 ETH

Outcome:

Boundaries and Repaying the Loan

Adding additional ETH collateral at lower price points would not materially move the liquidation price, and also result in overexposure to Aave.

Aave Exposure Limit

In general, for the purposes of this loan, we propose a hard threshold of 40% of the Capital Pool locked in Aave smart contracts - anything beyond this point should instead be used to repay the debt position instead.

Extremely Low Price Threshold

Furthermore, if the ETH price drops to $500 and approaches the liquidation threshold following the three collateral top-ups, we suggest paying off the loan using ETH instead of adding more ETH collateral to Aave.

There has to be a point where the ETH price continuing to drop results in cutting our losses rather than adding more and more collateral to Aave, otherwise we will:

- overexpose ourselves to Aave smart contract risk,

- overexpose ourselves to market risk resulting in the possibility of actually being liquidated or losing the entire Capital Pool.

The $500 threshold has not been encountered since November 2020. We believe that in order to achieve this price level again, the entire Ethereum ecosystem is likely in crisis and repaying the debt using ETH would be treated entirely as an emergency measure.

Therefore, the exact amount of repayment and assets used if ETH price falls below $500 is delegated to the Advisory Board.

Technical Practicalities of Increasing/Decreasing Collateral

ETH in the Capital Pool

There needs to be 3000 ETH set aside in the Capital Pool at all times to allow for a single threshold increase in collateral if required.

Increasing collateral

There are several steps involved in topping up the collateral using ETH from the Capital Pool:

- Make a request from the AB Multisig to receive ETH from the Capital Pool.

- Trigger an EOA transaction to transfer the funds.

- Convert the ETH to aEthWETH in the AB Multisig.

In order to top up the collateral before reaching the ETH price thresholds outlined above, the AB may choose to take some of the steps after being notified of the price approaching the threshold (see Notifications section below).

Decreasing collateral

It is possible to withdraw from the aEthWETH position to ETH in the Capital Pool in a single transaction.

In order to minimise the administrative burden when prices fluctuate near the price thresholds outlined, there are no strict triggers for when to remove the collateral from the position. Instead removing collateral is left at the discretion of the AB, whose members will take into account the following when deciding whether to decrease the collateral:

- Maintaining a maximum of $800 ETH/USD as the liquidation point

- Collateralisation ratio of the position, aiming for a minimum of 300%

- Requirements for ETH in other parts of the mutual, e.g. to pay claims or as liquidity for the RAMM

Notifications

The Foundation Engineering team will set up appropriate ETH price notifications to themselves and members of the AB so that the collateral-related transactions can be executed in good time. The notifications will occur in the following ranges, matching the collateral top-up and extremely low price thresholds as described:

- $1600 - $1700 ETH/USD

- $1250 - $1350 ETH/USD

- $1000 - $1100 ETH/USD

- $500 - $700 ETH/USD

Proposal Status

Open for review and comment until 17 July.

After 17 July, this NMPIP will be eligible to be put onchain for a full-member vote.