![]() oSaaT here, posting this as member of the Investment team.

oSaaT here, posting this as member of the Investment team.

Looking forward to hearing your thoughts on the proposal

Introduction

So far, the investments of the capital pool have been ETH-denominated.

The topic of asset/liability mismatch (ALM) pops up regularly (and rightly so) in the forum discussions.

See the latest forum post by Rei here: [RFC]: Matching Currency of Assets and Exposure

TLDR (on ALM)

- As the mutual has a majority of claims being bought in DAI, it would make sense to increase the portion of DAI-denominated investments at some point in time.

- However, as the gearing/leverage of the capital pool is still very low, there is no need to rush.

- For the past DAI-denominated claims, ETH was swapped for DAI in the days before claims payment as needed.

This proposal addresses this situation, with the main benefit to earn yields in the process.

Rationale

Objectives:

- Generate fees

- Increase DAI portion of the capital pool (to be able to meet liabilities in DAI, no matter how much ETH/DAI fluctuates)

To be clear, I’m giving slightly more weight to the first objective (‘fees’).

But slowly increasing the DAI allocation is a welcome benefit; also it allows us not to focus too much on the impermanent loss aspect of this AMM-based strategy.

Of the available universe of returns for the mutual to obtain, a Uniswap ETH/DAI position is appealing for a number of reasons.

- The yields are relatively high

- The position would accumulate DAI with rising ETH prices (and remain ETH-neutral in a down market)

As a side-note: this strategy allows the mutual to sell ETH for DAI programmatically, removing emotions from the decision (when to pull the trigger); it does so in a market with rising prices, which feels much better than when we were discussing it with ETH reaching new lows on a weekly basis.

Description of strategy

Given the objectives above, I suggest the capital pool should become a liquidity provider in the ETH/DAI pool(s), and start supplying ETH as a ‘single-sided’ LP.

LPing on Uniswap v3 could be an attractive solution for our capital pool, in general.

And especially as it solves the objective of DAI-denominated assets for the mutual, having yields high enough to compensate the much-dreaded ‘impermanent loss’ (IL) of an LP in Uniswap becomes less important a factor.

It is conceptually similar to entering a covered call position, but with no strike date, agreeing to sell our ETH at a DAI price in the middle of the defined range.

Resources:

- Uniswap v3 concentrated liquidity: Concentrated Liquidity | Uniswap

- Similarity to covered call explained here for example: https://twitter.com/charlie_defi/status/1616133079407394829

- Dashboards for visualization (rewards, impermanent loss)

https://defi-lab.xyz/uniswapv3simulator

https://app.apy.vision/uniswap-v3-positions (filter for WETH+DAI, add min nbr of days and min amount)

Investment strategy

=> Providing liquidity single-side with 100% ETH starting 1 tick above current price

A. Choosing a range:

- I suggest designing the position to become 100% DAI at ETH prices above $4,000.

- Why? close to all-time-highs, as the ETH price was above this level only for about 2 months at the end of 2021. This represents a justifiable medium-term target (150% increase off today’s prices at $1,600).

- Also, at prices above $4k, the ETH-denominated portion of the portfolio will have more than doubled in value, so this Uniswap investment would represent a smaller portion of the capital pool.

- Depending on the weight that the members choose to give to the diversification in DAI vs fees, we could also consider lowering the upper limit of the range

- eg half-way towards $4k

- there is always the possibility to split this “Uniswap v3 strategy” in several pools. Let’s say 50% with the $4k limit, and 50% with the lower limit…

B. Reinvestment:

- We should claim fees frequently (weekly or fortnightly)

- The DAI portion of fees should be sent to the capital pool (for future claims payment)

- The ETH portion of fees could be:

- either swapped for more DAI (aiming for $-denominated rewards)

- supplied as single-sided liquidity in the same pool 1 tick below current price (range tbd)

- also sent back to the capital pool

Proposal

Amount and duration of investment

Amount:

The proposal is for Nexus Mutual to invest 10% of the mutual’s current assets.

This represents investing about 16,000 ETH from the Capital Pool into Uniswap v3 ETH/DAI pool(s).

At the present time, this seems like an appropriate level where the risks to the overall soundness of the Mutual are limited (see Risks section), while obtaining a meaningful reward for our investment (see Rewards section).

Duration:

There is no set duration for the investment, with the caveat that the appropriateness of providing liquidity in these Uniswap v3 pools remains.

The longer we stay in the position (“in range”), the more fees we get.

Rewards & performance

Parameters

(as of January 23rd):

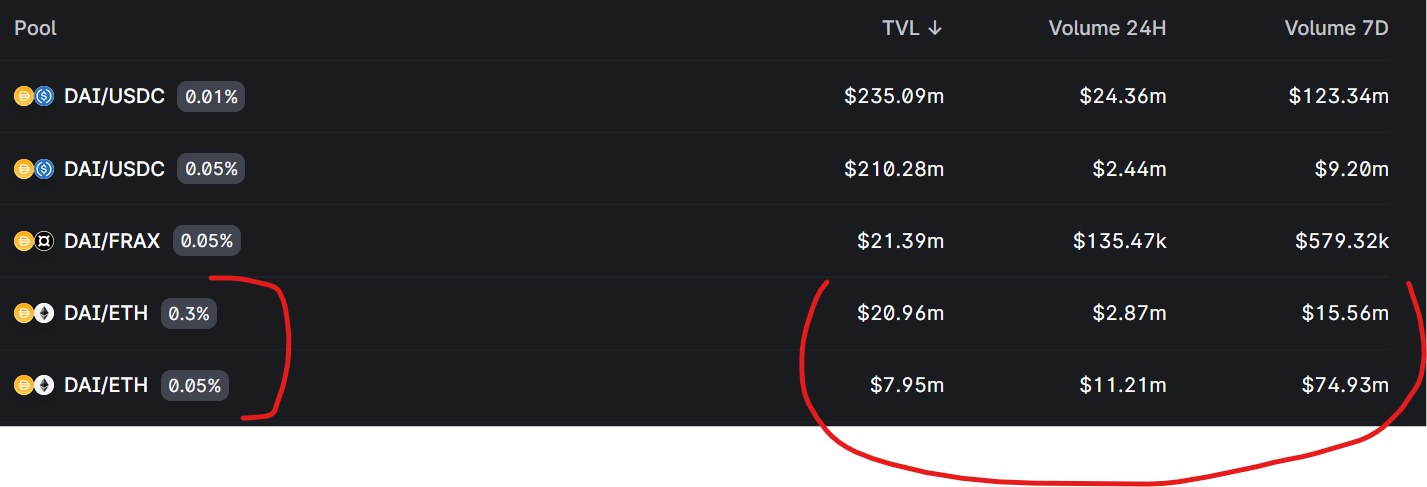

There are 2 main pools:

- ETH/DAI 0.3% pool with a TVL of ~$21m (liquidity in ETH per tick is about 75 ETH at current prices)

- the ETH/DAI 0.05% pool with a TVL of ~8m (liquidity in ETH per tick is around 7 ETH at current prices)

- the uniswap TVL data doesn’t include just-in-time liquidity. Depending on pools, there are ‘guesstimates’ it makes between 15% to more than 50% of the liquidity on Uniswap v3…

- volumes are quite volatile month-on-month, but do seem to be regularly at $10m per day between both pools, which means daily fees of more than $10k

- The cheaper pool has been getting a larger share of the volume, and this trend may accelerate.

Position size: 16,000 ETH (at ETH/DAI ~1600 => $25.6m)

Nexus Mutual would represent close to 50% of the liquidity.

I suggest we should split the investment across the 2 pools in the same ratio as current TVL (73%/27%).

It appears it would make more sense to put funds in the higher-fee pool, to avoid driving more volume to the lower-fee pool.

However, even at the current levels of liquidity, the 0.05% pool gets about 4X the daily volumes. This shouldn’t be ignored.

As investments of the mutual are more of the conservative and passive types, I suggest we follow the market signals and allocate based on the same ratio.

This could be reviewed on a monthly or quarterly basis (cf. Monitoring)

Rewards (in $ terms) are expected to be in the double-digit %; but these yields will be highly volatile, as they depend on several parameters:

- if the position is “in range”

- the trading intensity for this pair,

- competition from other DEXes

- and the behavior of additional LPs in these pools, especially Just-in-time liquidity providers.

To give some color - if all things stay the same:

In the ETH/DAI 0.3% pool:

- Volumes have averaged about $2m per day over the past month → daily fees of $6k

- Liquidity at the current tick is about $130k → 4.6% yield per day

- You need to dilute this figure by your own assumption of JIT liquidity (50%, more?..)

APY.vision (https://app.apy.vision/uniswap-v3-positions) has an interesting tool that allows us to see existing positions in all ETH/DAI pools, with filters on duration, amount. Most have an APY above 20%, but all with very different ranges.

See the links above to the other dashboard services which are quite well referenced; especially the one by Defi-Lab allows to compare strategies with different ranges and vs HODL (50/50 or 100% in one or the other token)

Monitoring

The position will be monitored on the basis of these parameters:

- total TVL

- Nexus share of TVL

- level of fees

- split of TVL across pools

- combined exposure with the amount of covers sold on Enzyme v4 and Uniswap v3

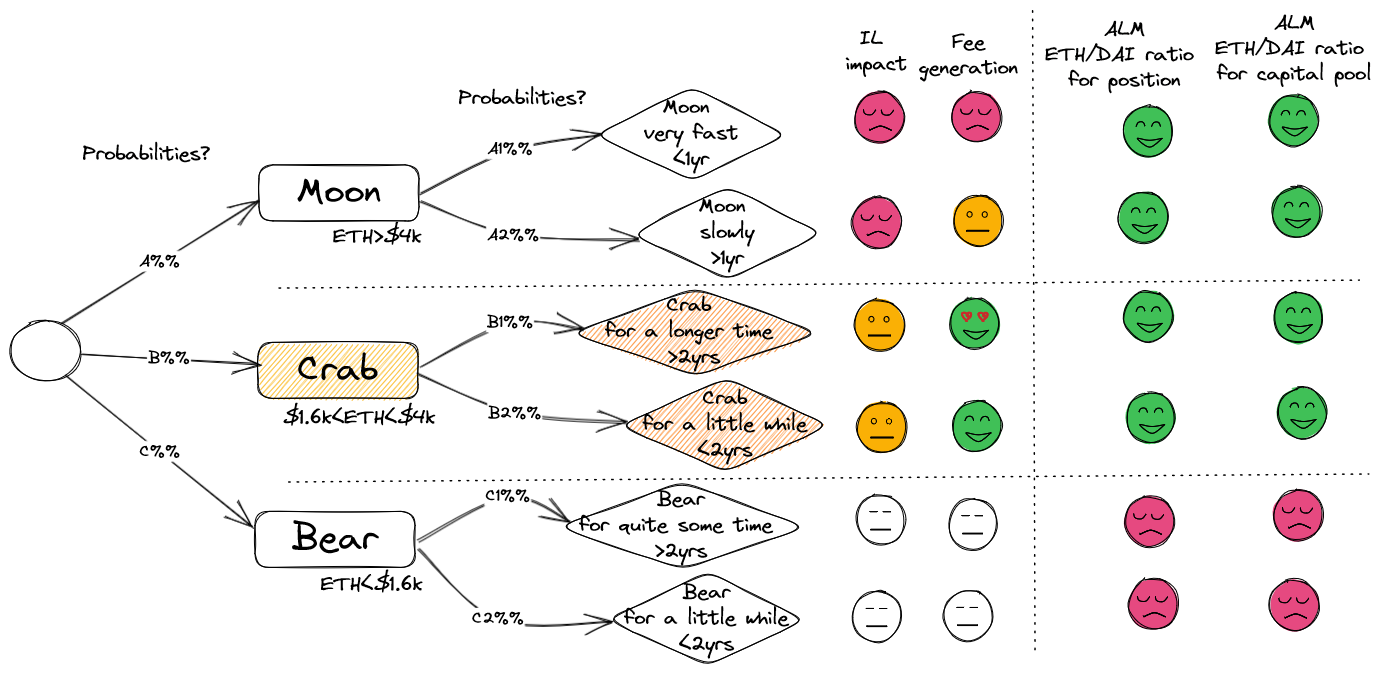

Outcomes

| Scenario | Description | Outcome for our ETH investment | Split ETH / DAI of Uniswap investment |

|---|---|---|---|

| Bear | ETH price remains below range and keeps dropping | 0 % yield | remains 100 / 0 |

| Moon | ETH breaks above $4k | Get swap fees as LP xx% | 0 / 100 (+ ETH & DAI fees) |

| Crab | ETH remains between $1.6k and below $4k | Get swap fees as LP xx% | a / 100-a (+ ETH & DAI fees) |

Risks

Nexus cover of protocol(s)

In order to avoid the compounding of risk within the mutual, Nexus should be minimising exposure so that total risk is capped to 20% of the mutual’s assets.

This is valid both for Enzyme v4 (active Protocol covers) and Uniswap v3.

Risks and Considerations for Nexus Mutual

This section discusses the risks for Nexus Mutual.

Based on the list of risks laid out in the investment philosophy, this strategy qualifies for the “lower risk” bucket:

| Risk | Comments (cf. Investment Philosophy) | Uniswap v3 ETH/DAI pools |

|---|---|---|

| Illiquidity Risk | Locking up capital for periods of time presents risk to the balance sheet should the mutual need those funds to pay claims. Note that the risk buckets here refer to liquidity in non-stressed scenarios. Stressed scenario liquidity is also a consideration but difficult to quantify. | Lower risk as the liquidity can be withdrawn immediately* (*Stressed scenario liquidity is also a consideration but difficult to quantify) |

| Basis Risk | The balance sheet is largely ETH denominated. ETH and DAI are effectively ‘cash.’ Investing in other tokens introduces basis risk. | Lower risk as fully ETH/DAI denominated |

| Protocol Risk (DeFi Safety Score) | Putting funds in a vault or liquidity pool to earn a yield opens up our funds to risk of loss from smart contract hacks | Lower risk as DeFiSafety score = 96% |

| Liquidation Risk | In the case of lending, Nexus collateral could be at risk of liquidation | Lower risk as no liquidation risk in strategy |

| Leverage | Refers to leverage of the balance sheet as a whole. Leverage may either be an explicit component of a particular strategy, or embedded leverage (Options, Futures, etc.) | Lower risk as no leverage in strategy |

| Counterparty Risk | Other additional qualitative & quantitative measures of counterparty risk may be used to assess investments & managers | Lower risk as exposures to single counterparty is below 20% |

| Economic risk | Some investments may result in losses on a short term basis, e.g. impermanent loss. | Lower risk as negligible possibility of loss (in this case impermanent loss would be a feature) |

Uniswap v3 is one of the highest-ranked protocol by the service DeFiSafety (96%)

This attests to the robustness of the contracts.These have been live for almost 2 years now and have a high bug bounty of $500k to encourage further reviews.

There are a few additional risks worth addressing:

- Impermanent loss

This risk is intrinsic to an AMM, especially in Uniswap v3 with concentrated liquidity

This risk is addressed above in the proposal with the rationale why - in most situations - it won’t be relevant for the mutual

- Liquidity / share of TVL

As the position would represent close to 50% of the liquidity in the ETH/DAI pools, this is worth considering.

DAI being an established ERC-20 and a top stablecoin listed on many exchanges, we do not expect these Uniswap pools to have a large impact on prices.

Increasing liquidity in these pools could also attract more trading volumes.

- DAI peg risk

This is a risk accepted by the mutual as DAI has been chosen as the stablecoin of reference for covers and claims.

The mechanisms in place at MakerDAO have withstood stress tests in the past.

Implementation:

Technical

The capital pool doesn’t have a direct integration with Uniswap v3, and claiming and reinvesting fees would pose a burden to the management of the capital pool.

For these reasons, we suggest using the Enzyme vault which was implemented for the Maple investment (link to proposal: Proposal: Allocate Capital to Maple Finance ).

Oracle

We need to know the size of the mutual’s position in these Uniswap v3 pools.

It is assumed that it would be handled by the Enzyme/Chainlink integration (to be confirmed).

Governance

The proposal will be put forward through the Nexus Mutual governance process after a period of review and feedback by the community.

If the governance process approves this investment, the implementation steps as outlined in the Technical section will be put in place by the Nexus Mutual team.