NMPIP: Grant Advisory Board the Power to Enter into Investment and Retrocession Agreement with Cover Re

Summary

Unity Cover—the manager of Staking Pool 5, which is run by some of the Nexus Mutual core team members—has been in discussions with Cover Re (“Re”) for some time over a potential investment and retrocession deal.

I am proposing that the Mutual enter into an investment and retrocession agreement with Re, which would require members to grant the Advisory Board the power to:

- Enter into investment agreements with Re on behalf the Mutual

- Swap $15m worth of ETH into stablecoins, $12m for the investment and $3m for collateral

- Set up a trust account held in Terrapin’s name for the Mutual

- Transfer the stablecoins for investment to Re and collateral into the trust account

- Whitelist USDC and a newly developed “Funds Withheld Token” as payment tokens for the Mutual

- Agree to final terms with regard to investment, collateral accounts, and funds withheld terms with Re provided they are consistent with the descriptions provided below

I present the details of this potential deal for members to discuss and share their opinions ahead of an all member no-action vote.

Rationale

Re is a Cayman Islands-based company that reinsures a variety of business lines including aviation, business owners, commercial multi peril, personal and commercial auto, professional liability, and workers compensation, among others. These business lines are very stable relative to the business that Nexus Mutual has written previously, as Protocol Cover and other cover products have, historically, been more binary (i.e., resulted in either minor or quite large claim payouts).

Re is in a position where it can significantly grow its premium volume but requires additional capital to do so. On the other hand, Nexus Mutual has underwriting capital ready to deploy and is looking to increase cover volumes. These strategic aims are complementary and form the basis of the deal structure presented in this proposal.

If the Mutual were to enter into an agreement with Re, members could expect to pay a stable level of claims every year and the profit margin would be much more predictable.

Re has attached $45M in premium volume so far this year. It is committed to complete on-chain transparency as it pertains to transactions and proof of reserves between itself and insurance companies it supports. Their team is composed of the former founders and engineering leaders of Cover, a national insurance business in the US which launched out of Y Combinator in 2016. Reinsurance operations are headed by the former CEO of Willis Programs, a $5B underwriting entity, and the founding Chief Actuary of Greenlight Re.

Specifications

The deal has two main components:

-

An investment of $12m into Cover Re SP1

-

Retrocession Cover deal where Re shifts 15% of their underlying risk to Nexus Mutual

Glossary

-

Funds Withheld Basis. Notional accounting basis where liabilities are transferred but cash payments follow later once the actual claims/losses are known and are closer to being final.

-

Insurance Float. Assets an insurance company holds are called the “float”, and an insurance company puts these assets to work and earns investment earnings on this in the meantime.

-

Margin. Premiums (or cover costs) less claims.

-

Gross Premium. Premium paid by the end insurance user, usually the retail client.

-

Net Premium. The premium or cover cost paid to Nexus Mutual after taking out expenses and profit margins for both the insurance company and Re.

-

Retrocession. Where a reinsurance company transfers risk to another company (another reinsurer or Nexus Mutual)

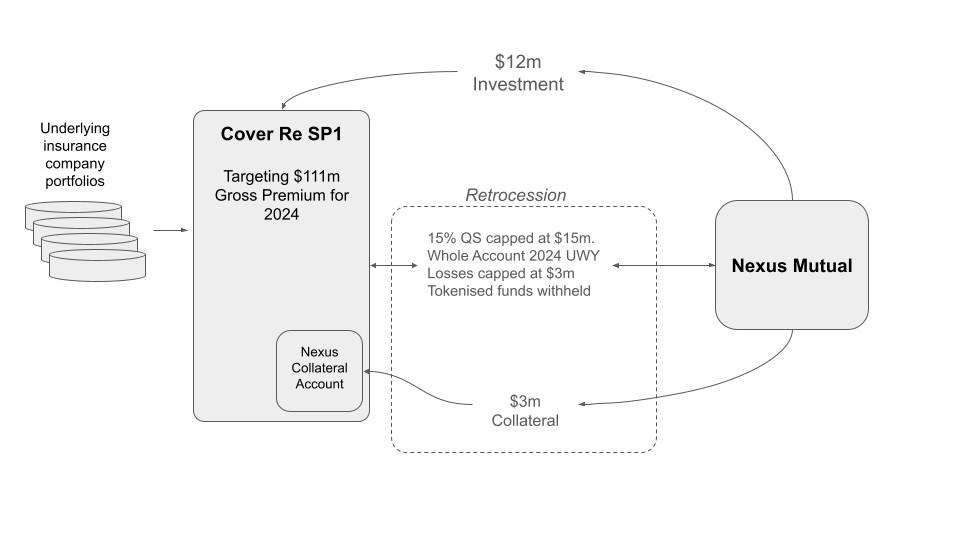

Investment into Cover Re SP1

The first component of the deal would be an investment in Re’s open-ended fund, whereby any funds contributed are locked for a period of at least one (1) year and can be redeemed thereafter, though we would expect funds to be locked for multiple years to support the strategic partnership. Per Unity Cover’s discussions with Re, the proposed start date for this investment is 1-Jan-2024.

Returns on the investment into Re are expected to be in the 18%-22% range, which is driven by expected profit margins on the reinsurance business line, as well as holding the insurance float in US treasuries. These returns are variable as they are linked to the underlying performance of the Re business. While unlikely, it is possible that the entire investment is lost if claims experience is very poor. On the other side, positive claims experience will result in additional returns.

This requires two main aspects for members to consider.

- Willingness to sell ~$12m of ETH for stablecoins

- Attractiveness of the Re investment

Retrocession into Nexus Mutual

The second component of the deal would involve Re entering into a “retrocession” arrangement (i.e., the insurance term where a reinsurer transfers risk), whereby Nexus Mutual would receive 15% of the underlying business for 2024 underwriting year capped at $15m gross premium. On a net premium basis we would expect Nexus Mutual’s revenue to increase by ~$10.8m (this is the cost of cover paid each year). The expected margin on this deal would be lower but much more stable at $1.7m (with approx. $0.5m coming from cover costs less claims and the remaining $1.2m coming from interest/earnings on cash flow). Total losses would be capped at $3m above net premium.

In order to access this deal, Re must obtain approval by the Cayman Islands Monetary Authority (CIMA), as Nexus Mutual is not a licensed insurer/reinsurer. Unity Cover has been working with Re behind the scenes on this approval process and have received positive indications from CIMA this is likely to be approved if the following conditions are met:

-

Deal operates on a “funds withheld” basis, meaning cover costs are paid on a delayed basis once the claim experience has become clear (likely over a 2-4 year period).

-

Collateral of $3m is posted in a trust account owned by Nexus Mutual at the call of Re should the Nexus Mutual cover not pay out.

In combination, these two requirements essentially reduce/remove the credit risk associated with Re interacting with Nexus Mutual’s discretionary cover.

If approved, this would be quite an achievement for the Mutual, as it would demonstrate that the Mutual’s on-chain capital can interact with TradFi insurance companies, and this deal could serve as a blueprint for future deals.

It would also demonstrate there is a route forward for “wrapping discretionary cover” with a traditional insurance contract, which could open Nexus Mutual’s addressable market quite considerably. MakerDAO and other DeFi protocols are exploring tokenised RWAs— a deal such as this one would be the equivalent for the insurance world. Members should consider this potential strategic value over and above the raw deal terms.

Technical Requirements for the Investment into Cover Re SP1

The following engineering work would be required:

-

Creation of a token that represents the off-chain investment in the Capital Pool

-

Creation of an oracle that would be updated once per quarter and reflect the performance of the investment

Technical Requirements for the Retrocession into Nexus Mutual

The following engineering work would be required:

-

Creation of a token that represents the trust funds held off chain as collateral (similar to approach for the investment)

-

Create a funds withheld payment token named “nexusUSD” (working title) that Re can use to pay cover costs and receive any subsequent claim payments in until the resulting profit on the deal can flow into the Capital Pool (funds withheld). The Nexus Mutual Advisory Board would have the authority to mint “nexusUSD” to Re to pay cover costs.

Proposal Status

This proposal is open for comment and will close after a minimum of 14 days from the date of this posting.

The proposed timeline of this NMPIP and the on-chain governance vote is shared below.

-

23 November 2023. Post NMPIP on the Nexus Mutual governance forum for members to review and comment on.

-

7 December 2023. NMPIP is put on chain for an all member no-action governance vote, where voting will be open for three (3) days. Voting will come to a close on 20 December 2023.

-

11 December 2023. The outcome of the NMPIP will be subject to a 24-hour cool-down period.